Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  BOJ Governor Kazuo Ueda Hints at Rate Hike as Inflation Pressures Build

BOJ Governor Kazuo Ueda Hints at Rate Hike as Inflation Pressures Build  RBA Rate Hike Outlook: Impact on AUD/USD and ASX 200

RBA Rate Hike Outlook: Impact on AUD/USD and ASX 200  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  RBA Raises Interest Rates to 4.35% Amid Rising Inflation Risks and Middle East Tensions

RBA Raises Interest Rates to 4.35% Amid Rising Inflation Risks and Middle East Tensions  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts

Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts  ECB Rate Outlook: Ceasefire Eases Pressure but Hikes Still Expected in 2026

ECB Rate Outlook: Ceasefire Eases Pressure but Hikes Still Expected in 2026  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  BOJ Holds Interest Rates at 0.75% as Policymakers Signal Growing Inflation Concerns

BOJ Holds Interest Rates at 0.75% as Policymakers Signal Growing Inflation Concerns

While Christmas is fast approaching, this week is still a busy one for both policymakers and financial markets. Fed is scheduled to announce its funds rates on 13th Dec that is most likely to hike by 25 bps and ECB to announce its monetary policy on 14th, and later in the week, the EU summit is expected to confirm that ‘sufficient progress’ has been made to push Brexit talks forward to the next stage.

As the ECB edges towards normalization, an undervalued euro has room to rise further, the European central bank joined in and a significant dollar rally was underway.

The FX market reaction to the US labor market report on Friday was an ideal illustration of how the market operates at present. Just as a reminder: the number of new jobs created in November (which used to be the most important data release on any FX traders monthly data calendar) came in well above the expectations of the large majority of analysts at 228k (media of expectations 195k). That means the real economic data would have justified USD appreciation, but in fact, the market’s initial reaction was: USD weakness.

Hence, in this seesaw sentiments, options straddles deploying +0.51 delta ATM call and -0.49 ATM delta puts at net debit. The strategy is likely to hedge underlying spot FX price risks in the below OTC sentiments regardless of the above stated driving forces.

The current slope is at shy above 7.25% which is below prior peaks whereas historical vols are near 6.9%, our intent is to begin legging into EUR 1Y ATMs perhaps 0.3-0.5 vols lower from the current market once we see a 2-handle print on the curve.

Given the depth of the Euro option market, owning EUR vol from near two-decade lows constitutes the most scalable FX risk premium normalization trade for 2018 in our view.

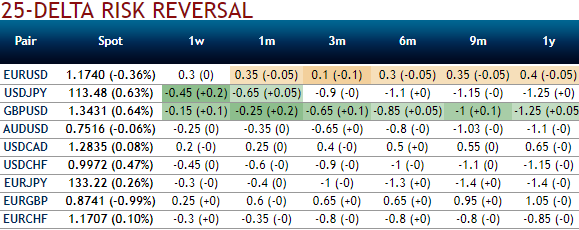

While please be noted that the recent shift in risk reversals are flashing negative number. However, the hedging interests for bullish risks remain intact. This standpoint is substantiated by positively skewed IVs of 1m tenors.

Hence, alternatively, those who are dubious about euro’s bullishness, the 3m EURUSD call spread of net delta around 0.39 is advocated at net debit.

Contemplating above OTC market reasoning and fundamental factors we think further upside risks are on the cards amid minor hic-ups, as a result we reckon deploying longs on ITM call option with delta being at around +0.61 in hedging strategies are worthwhile and to reduce the cost of hedging we would also like to write over OTM puts as the northward forecasts remain maximum upto 1.21 mark.

Currency Strength Index: FxWirePro's hourly EUR spot index is gaining traction displaying shy above 27 levels (bullish), while hourly USD spot index was at 26 (bullish) while articulating (at 12:02 GMT). For more details on the index, please refer below weblink:

http://www.fxwirepro.com/currencyindex.

FxWirePro launches Absolute Return Managed Program. For more details, visit: