US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure  Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening

South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow  ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus

ECB Expected to Hold Rates as Middle East Tensions Keep September Hike in Focus  Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

The industrial production in the UK dropped by 1.3% MoM in October, dramatically undershooting our and consensus expectations, building on a 0.4% MoM contraction in September. Within overall production, manufacturing output also dropped by 0.9% MoM, more than reversing a 0.6% MoM gain in September.

It was the sharpest decline since September 2012, as mining and quarrying fell sharply, dragged by oil and gas extraction; and manufacturing output also shrank, mainly due to a contraction in pharmaceuticals. Furthermore, sterling’s export-supportive declines notwithstanding, an export-led boost and rebalancing away from services and the consumer still seems relatively distant on these data.

Just until recent times, the many analysts had been expecting the RBA to sit tight at 1.5% cash rate for some time and the central bank also delivered as anticipated.

But in contrast, the Australian economy unexpectedly declined 0.5 pct in the Q3’2016, compared to an upwardly revised 0.6 pct growth in the June quarter and missing market consensus of a 0.3 pct expansion.

As a result, the RBA’s monetary policy would remain expansionary; a more easing cycle is on cards. In other words, the Aussie central bank members can make the most of the summer break, rate hikes in Australia are not foreseeable for now which would imply that the more bearish pressures on AUD.

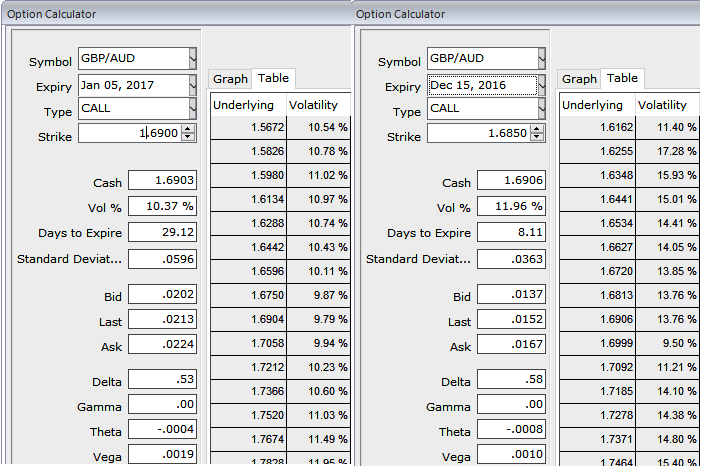

Hedging Framework:

3-Way Options straddle versus Call

Spread ratio: (Long 1: Long 1: Short 1)

Rationale: The current implied volatility of GBPAUD 1w ATM contracts is just shy below 12%, and it is likely to shrink below 10.5% for 1m tenors as shown in the IV nutshell, shrinking IVs is conducive for over-priced option writers. Option writers of expensive calls with 1m expiries would be on competitive advantage.

The execution of the strategy: Go long in GBPAUD 3M at the money -0.49 delta put, long 3M at the money +0.52 delta call and simultaneously, Short 1m (1.5%) out of the money call with positive theta or closer to zero.