Paraguay Holds Interest Rate at 5.5% as Inflation Remains Stable Amid Global Uncertainty

Paraguay Holds Interest Rate at 5.5% as Inflation Remains Stable Amid Global Uncertainty  BOJ Holds Interest Rates at 0.75% as Policymakers Signal Growing Inflation Concerns

BOJ Holds Interest Rates at 0.75% as Policymakers Signal Growing Inflation Concerns  BOJ Governor Kazuo Ueda Hints at Rate Hike as Inflation Pressures Build

BOJ Governor Kazuo Ueda Hints at Rate Hike as Inflation Pressures Build  Kevin Warsh Advances Toward Fed Chair Role Amid Political Tensions

Kevin Warsh Advances Toward Fed Chair Role Amid Political Tensions  South Korea Central Bank Signals Inflation Concerns as Oil Prices Surge

South Korea Central Bank Signals Inflation Concerns as Oil Prices Surge

After very busy recent weeks that contained 3 major central bank meetings and important turn-of-the-month data, FX markets continue to be imprudently US centric and mostly intensive on the repricing of hopes of Trump policies, rather than driven by more concurrent macro events. While much of the positioning and short-term valuation overshoot from the start of this year has unwound, the dollar remains vulnerable to Trump policies. In particular has been Trump’s growing direct engagement with international currency politics in a way that threatens to upset the status quo and drive a further leg down in the dollar.

Flow of funds data show that the equity withdrawals by G4 nonfinancial corporates remained very strong in Q3 last year, only modestly below its record high seen in Q2.

The last time net purchases of equity funds were below dividends reinvested was during the euro debt crisis years of 2011 and 2012 and during the Lehman crisis of 2008.

Into 2017, a projected increase in equity offerings is likely to be offset by stronger equity withdrawals as repatriation bolsters US share buybacks.

The dollar index has retraced 45% of the Trump rally, but we believe risk-reward favours a deeper setback vs those pairs that have lagged, most notably JPY. Tax policy including border-adjustment is a very slow work-in-progress; FX policy has the potential to be far more fluid.

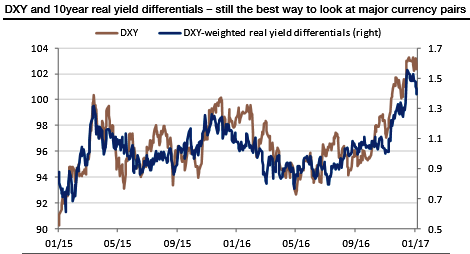

Real bond yields continue to drive currency trends after the FOMC hiked rates in last December month, the dollar’s having a bit of a wobble. There are echoes of the dollar’s correction in the first half of 2016, partly because the peak in real US yields is almost identical to what we saw in January 2016, but we still expect to see nominal US yields reach 3%, real yields reach 1% and the DXY index rally by a further 5% between now and the end of President Trump’s first hundred days in office.

Over the last few years, the relationship between FX rates and interest rate differentials has shifted. The chart above shows DXY-weighted 10-year real yield differentials next to the DXY index. Not perfect, but not bad. This fit is better than for 10-year nominal yields, and better than for 10 or 2 year swap differentials for that matter and for now, it’s going to remain a corner-stone of how we think about FX trends in 2016.

This relationship is interesting and useful but of course, it largely swaps one problem – trying to forecast FX trends by looking at the wrong things – while creating another – trying to forecast trends in real yields.