Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks

BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  Denmark Central Bank Intervenes to Support Krone Peg Against Euro

Denmark Central Bank Intervenes to Support Krone Peg Against Euro  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why

Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

We continue to envisage a phased decline in EURCHF to 1.03 by year-end predicated on a relaxation in the SNB’s very aggressive intervention tactics once the immediate threat of exchange rate instability spilling over from the French election has passed.

We do not expect a benign outcome to that vote to sponsor an underlying weakening in the franc since the upward pressure on CHF clearly predated the emergence of political stress in the Euro area and is caused instead by Switzerland’s positive balance of payments position.

The basics of that situation remain intact –an inadequate interest rate differential between CHF and EUR to generate sufficient private-sector capital outflows to recycle the large current account surplus. The current a/c surplus was 10.8% of GDP in 2016, in contrast to which unhedged private capital outflows were less than 1.5% of GDP.

Our longstanding bullish view on CHF has been motivated by the decent domestic data both on the activity and inflation front which should eventually result in reduced FX intervention activity by the SNB.

The past week reinforces the view that activity data remains strong in Switzerland with the KOF leading indicators beating consensus to make a new 3-year high.

The SNB has admittedly continued to intervene in FX markets — it sold CHF 2.9bn last week even though EURCHF was above 1.07 — perhaps indicating a more active approach to engineer a squeeze in the cross.

However, interventions are likely to become increasingly given the global political climate.

The Treasury is due to release its semiannual report on currencies on April 14th and Switzerland is again expected to meet the thresholds for two out of the three criteria that the Treasury uses to identify currency manipulators.

Stay short EURCHF in cash (first entered 1.0720 since March). Marked at 0.3%.

The primary reason is that there is no compelling economic rationale for the SNB to frustrate all of the CHF appreciation that would be justified by Switzerland’s juggernaut current account surplus. We stay short EURCHF in cash and add downside in USDCHF through a 3-month put spread.

Since we sold, 3m vols have dropped by 1.7 points and the 3-mo risk reversal has tightened from -3.4% to-2.5%.

Hold a 2m 1.0050 - 0.97 USDCHF put spread.

Our choice of a put spread is motivated by:

1) The French election calendar should prevent USD/Europe from running away ahead of the second-round presidential runoff on May 7 and the Assembly elections on June 11 and 18, and

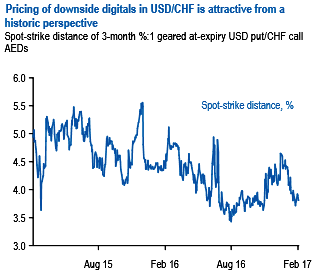

2) Digitals are reasonably priced for downside in USDCHF. The digital profile can be replicated with a vanilla spread (refer above chart).

3) We would like to favor optionality in USDCHF as ATM IVs are comparatively better over EURCHF.