BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence

Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence  Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey  Economic pessimism has set in – but there are reasons for Australians to be hopeful

Economic pessimism has set in – but there are reasons for Australians to be hopeful  BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks

BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  RBI Hits Pause as Geopolitical Storm Clouds Gather

RBI Hits Pause as Geopolitical Storm Clouds Gather  Europe Heatwave Creates Growth Opportunity for Carrier, Trane, and Johnson Controls, Citi Says

Europe Heatwave Creates Growth Opportunity for Carrier, Trane, and Johnson Controls, Citi Says  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

GBP has deferred the impending sell-off risk due to several upside breaks, however this seems to be only postponing the looming setback.

The GBPJPY has been volatile, edged higher briefly to just shy above $135 after bottoming out at 123.298 level in mid-May, as the reports of a Brexit deal agreement also cushioned the bulls. Currently, trading with little exhaustiveness due to pandemic turmoil coupled with Brexit saga back in action, still, it is well up from last week’s lows.

Even so we reckon that it worthwhile increasing our bearish beta to GBP through re-selling GBPJPY (our single most successful trade to date this year).

This week, BoJ and BoE monetary policies, UK CPI & PPI figures provide the most comprehensive indication yet of the economic impact of the lockdown.

While the UK Services PMI was revised higher to 29.0 in May 2020 from a preliminary estimate of 27.8 and compared to April's record low of 13.4. It was still the second-lowest reading since the survey began in July 1996, with travel, tourism and leisure firms being the most affected amid the coronavirus pandemic. New business continued to fall at a sharp rate, with new export work falling rapidly despite sporadic reports of rising demand in the Asia-Pacific region and new online sales initiatives. In addition, employment decreased at the second-steepest rate on record.

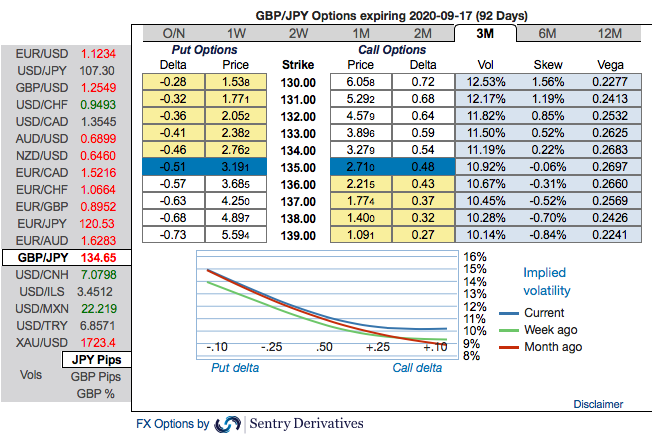

GBP/JPY OTC outlook and Hedging Strategy: The implied volatility of this pair that display the highest number among entire G7 FX universe.

While the positively skewed IVs of 3m tenors signify the hedgers’ interests to bid OTM put strikes up to 130 levels (refer above nutshell).

Accordingly, put ratio back spreads (PRBS) are advocated on the hedging grounds. Both the speculators and hedgers who are interested in bearish risks are advised to capitalize on current abrupt and momentary price rallies and bidding theta shorts in short run, on the flip side, 3m skews to optimally utilize delta longs.

The execution: Capitalizing on any minor upswings , we advocate shorting 2m (1%) OTM put option (position seems good even if the underlying spot goes either sideways or spikes mildly), simultaneously, go long in 2 lots of delta long in 2m ATM -0.49 delta put options (spot reference: 134.712 levels while articulating). The position is a spread with limited loss potential, but varying profit potential. The degree of profit relies on the strength and rapidity of price movement.

In addition, we advocated shorts in futures contracts of mid-month tenors alternatively with a view to arresting potential dips, since further price dips are foreseen we would like to uphold the same strategy by rolling over these contracts for July month deliveries.

While on trading grounds, buy GBPJPY 2M ATM straddle vs Sell GBPUSD 2M ATM straddle, equal notionals. Courtesy: Sentry, Lloyds & JPM