China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics

The euro slipped only moderately yesterday in reaction to the weaker than expected ifo index, with the data not actually being as weak as it might have seemed at first glance. In the current market environment of increased risk aversion the euro too seems to be in demand as a safe haven. The currencies that were hit quite hard instead in the G10 universe were the AUD (see below) and also the Scandinavian currencies which were affected by general uncertainty as well as increased economic risks in the euro zone.

Sterling on the other hand was amongst the winners yesterday. At present the currency is likely to be benefitting mainly from the recent fall in rate cut expectations. And indeed the stronger than expected PMI for January rekindles hopes of a certain economic recovery, which in turn reduces the need for monetary policy easing. It is still uncertain though to what extent the relief about the UK elections and an orderly Brexit will continue, as Brexit is far from over yet. Above all it is still unclear how close the trade relations between the UK and the rest of the EU will be once the transition period projected for year-end expires. As a result the uncertainty for businesses remains high. With this in mind the rise of the PMI might easily turn out to be a one-off.

The downside risks for Sterling thus remain considerable as GBP headroom is capped as investors have no clarity about the most important issue that will determine the economic consequences of Brexit - the future trade deal - albeit Johnson’s WA envisages a looser set of arrangements than May’s ill-fated deal.

We set the landing zone for cable in the event of a comfortable Conservative victory in the low 1.30s. Now we clearly didn’t reckon with the outpouring of speculative enthusiasm that would greet the delivery of an emphatic 80 seat Johnson majority, the largest for the Tories since Thatcher in 1987.

Nevertheless, the spike to 1.35 on election night proved very much an overshoot and GBP has since reverted to the low 1.30s, in line with our original projections. Despite Johnson’s surprisingly large majority, we see no basis to revise our GBP projections, these have been unchanged for quite a few months now.

Moreover, there is still the risk of an economic cliff-edge at the end of 2020 if Johnson honours his commitment not to extend the one-year transition.

Our assumption is that Brexit is the dominant issue for markets and so broader economic policies will be secondary for the exchange rate. GBP will likely take its directional cue from the read-through to Brexit whereas the size of the move will be augmented or moderated by the government’s broader policy platform.

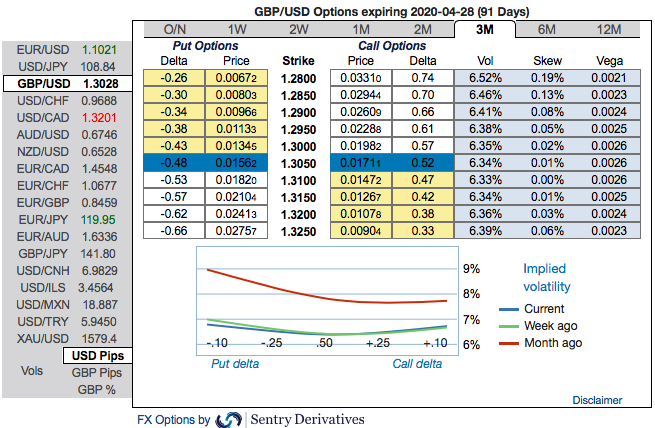

Strategy (Debit Put Spread): Contemplating above factors, wise to deploy diagonal options strategy by adding short sterling via a limited loss tail hedge: Stay short a 1M/3W GBPUSD put spread (1.33/1.29), spot reference: 1.3038 level.

The Rationale: Observe the 3m GBP skews that has stretched on both the sides, hedgers have shown interests on both OTM Calls and OTM Put options.

To substantiate the downside risk sentiment, risk reversal numbers have still been signalling bearish hedging sentiments in the long run amid minor bids for upside risks. Hence, we advocate the diagonal options strategy on both hedging and trading grounds. Courtesy: Sentry, JPM & Commerzbank