UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  BTC Flat at $89,300 Despite $1.02B ETF Exodus — Buy the Dip Toward $107K?

BTC Flat at $89,300 Despite $1.02B ETF Exodus — Buy the Dip Toward $107K?  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges

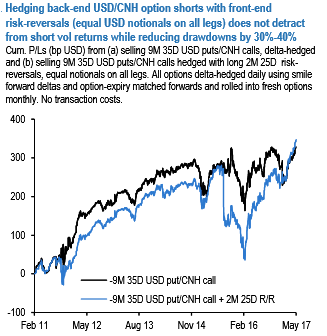

A steeply upward sloping CNH vol curve in the 3M-1Y segment motivates forward vol selling at a substantial premium to spot ATM vol. The steepness of the vol curve is substantial for the level of base vols and worth milking via +2M/-9M gamma-neutral calendar spreads in the absence of a liquid forward volatility (FVA) product market. The pushback against CNH vol selling is not difficult to anticipate.

The most obvious argument is levels: depressed front-end CNH vol (1M @ 3.0, 2M @3.3) raises question marks around the wisdom of fresh shorts, especially at a time when the policy pendulum is once again swinging in the direction of credit tightening after a year of heavy deficit spending. The argument is legitimate, though there is a counter -case to be made that such considerations may prove secondary to the overarching, widely broadcast desire for systemic stability in the lead-up to the all-important NPC plenum in Q4 this year.

While a misfiring White House policy engine and tepid ranges on the dollar have helped tame overall currency vol this year, it is worth noting that CNH vols have fallen markedly even relative to other EMs –the ratio of CNH / EM VXY realized vols is near 3Q16 lows when RMB stability was prioritized in the run up to SDR inclusion – indicating an appreciable degree of Chinese policy interest in dampening currency volatility.

The flatness of the CNH vol term structure beyond the 1Y point also motivates carry-earning calendar spreads, preferably in the direction of slow-burn currency weakness that is the baseline outcome in the minds of many investors.

For pure vol investors, delta-hedged-9M straddle vs. +18M 25d strangle calendar scan exploit this flatness while alongside the cheapness of CNH flies (even adjusted for ATM vol levels) that increase the appeal of short straddle/long strangle packages.

For directional investors not given to frequent delta-hedging, we propose -9M 7.05 vs. +18M 7.15 USD call/CNH put calendars that accrues positively to the over the life of the short leg while awaiting a renewal of RMB weakness, possibly after the November plenum.