U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts

Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Eurozone Recession Risks Rise as Middle East Conflict Threatens Growth, ECB Official Warns

Eurozone Recession Risks Rise as Middle East Conflict Threatens Growth, ECB Official Warns  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  ECB Signals Possible Interest Rate Move if Inflation Outlook Fails to Improve

ECB Signals Possible Interest Rate Move if Inflation Outlook Fails to Improve  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing

Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  OECD Sees Bank of Japan Raising Interest Rates to 2% by 2027

OECD Sees Bank of Japan Raising Interest Rates to 2% by 2027

NBP held its first rate-setting meeting of the year today: The National Bank of Poland held its reference rate at a record low of 1.5 pct on January 10th, 2018, as widely expected. Also, the Lombard rate and the deposit rate were kept unchanged at 2.5 pct and 0.5 pct, respectively, and the rediscount rate was left at 1.75 pct. The central bank ended an easing cycle in March 2015.

The governor stuck to his stance that rates are likely to remain flat until the end of 2018. Since that time, data have in fact supported a dovish stance: inflation has dropped back to below-target 2% in December and core inflation remains subdued at just c.1%.

Additionally, the MPC no longer refers to a tightening labor market as a source of risk. The MPC current balance between doves and hawks suggests that no rate hike is likely until H2’2018.

The zloty has staged a significant rally over the past month, but this has been part of a broader rally in EMFX – the zloty has not outperformed peers such as the forint over the past month. We forecast EURPLN to gradually rise through this year.

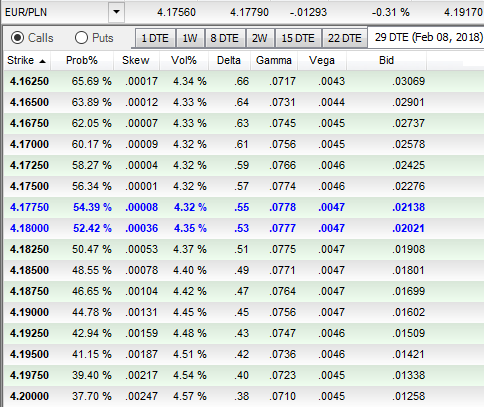

Accordingly, we’ve already advocated credit call spreads a month ago on 5th of last month, please go through below weblink for further reading on the same:

Well, short leg so far has functioned very well as per its objective. Now, it is on the verge of fetching positive cashflows in long legs.

At spot ref: 4.2046 back in 5th December, we had advocated shorts in EURPLN and 1m2m diagonal call spread (4.1650/4.2650). The underlying spot FX trend and IV skews of 1m tenor have been favorable to long OTM calls.

At prevailing spot rates at 4.1857 levels, we uphold longs in OTM calls on hedging grounds.