BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei

BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei  China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt

Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt  Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  Indonesia Central Bank to Draft New Regulations After Expanded Economic Growth Mandate

Indonesia Central Bank to Draft New Regulations After Expanded Economic Growth Mandate  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

It was primarily the Brexit that cast its shadow over the Bank of England's monetary policy so far. The central bank had clearly signaled that normalization of its monetary policy over the medium term depended on an amicable outcome to the negotiations. But in view of global trends towards a looser monetary policy, this plan is now likely to be obsolete. Admittedly, some MPC members had recently still argued in the other direction, namely that the market could underestimate BoE interest rate hikes in the face of increased inflation risks. But even if there is no hard Brexit, it is doubtful that the BoE will raise its interest rates in the foreseeable future, while the Fed and ECB are moving in the opposite direction. The question that is more likely to arise is whether the BoE is not eventually following the trend and also considering a loosening. This would be a completely new burden for Sterling. At the same time, Brexit uncertainty, which will probably last until the end of October - the next Brexit deadline - is limiting the British currency's appreciation potential. Sterling bulls are facing truly hard times these days.

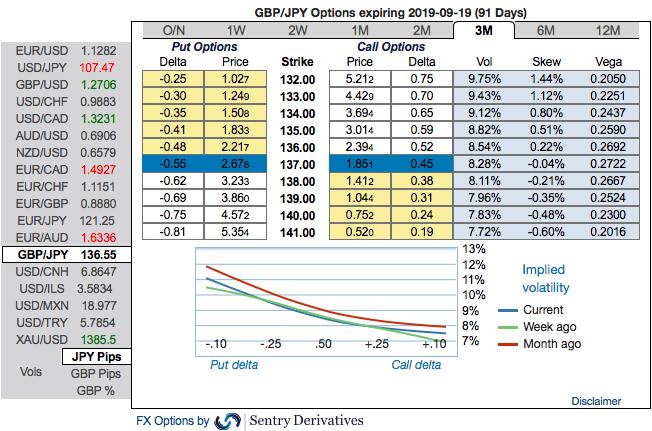

We know GBPJPY is the major trend is still weaker (see above chart) but the traders bother for the profit maximization.

It all depends on how much return that your strategy has fetched you when your trade convictions are right, not that how many times your trade guesses are right. Well, in that perspective, before proceeding further let’s just quickly glance at OTC outlook and suitable strategy for GBPJPY swings.

OTC outlook and Hedging Strategy: Please be noted that IVs of this pair that display the highest number among entire G7 FX universe.

While the positively skewed IVs of 3m tenors signify the hedgers’ interests to bid OTM put strikes upto 132 levels (refer above nutshells evidencing IV skews). Hence, it is wise to capitalize on momentary upswings of GBPJPY and deploy OTM put writing.

Accordingly, put ratio back spreads (PRBS)are advocated on the hedging grounds. Both the speculators and hedgers who are interested in bearish risks are advised to capitalize on current abrupt and momentary price rallies and bidding theta shorts in short run, on the flip side, 3m skews to optimally utilize delta longs.

The execution: Capitalizing on any minor upswings , we advocate shorting 2m (1%) OTM put option (position seems good even if the underlying spot goes either sideways or spikes mildly), simultaneously, go long in 2 lots of delta long in 2m ATM -0.49 delta put options (spot reference: 138.19 levels).

The rationale for PRBS: The position is a spread with limited loss potential, but varying profit potential. The degree of profit relies on the strength and rapidity of price movement. The position uses long and short puts in a ratio, such as 2:1 or 3:2, to maximize returns as explained above. In most long/short spreads, you make money if the spot fx moves, but you lose if it remains in the middle “loss zone.”

Every underlying move towards the ITM territory increases the Vega, Gamma, and Delta which boosts premium. As you could observe spot GBPJPY keeps dipping, these delta longs would become in the money, while these derivatives instruments target further bearishness of this pair. Courtesy: Sentrix & Commerzbank

Currency Strength Index: FxWirePro's hourly GBP spot index is flashing 53 (which is bullish), while hourly JPY spot index was at -27 (mildly bearish) while articulating (at 11:09 GMT).

For more details on the index, please refer below weblink: http://www.fxwirepro.com/currencyindex