Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields

Mexico-induced reprisal of risk in Brazil best expressed via long USDBRL skews / vols hedges: Is Brazil bound to go down the same slippery path of some of the other recent populist governments? It’s yet to be seen. BRL skews have rolled off the election premium, narrowed down back to a long-term average and to only a touch above the year start level. While from the systematic trading standpoint BRL is only marginally different from the above MXN analysis, the risk from a reprisal of this week’s AMLO surprise in Brazil keeps us defensive and biased to long vol and long skews. While delta-hedged 1*1.5 ratio put spreads performance wasn’t exactly stellar (when compared to the outstanding 1*1.5 ratio call spreads), selling OTM puts is a good way to subsidize long vol lean.

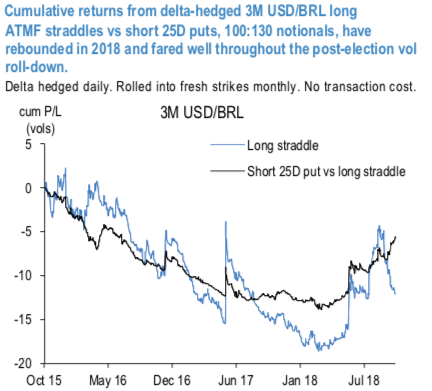

Namely, a long straddle vs short 25 delta OTM USDBRL put in 130:100 notionals structure (refer above chart) would offer a natural protection in case of further shift lower in BRL vol surface.

Also, in the event of upbeat, risk-on, sentiment (i.e. post-election honeymoon period), which could gradually drive spot lower, soft realized vol with spot at the short leg should benefit the trade.

Returns from a 3M USDBRL long ATMF straddle vs short 25D put (delta-hedged) have rebounded in 2018, fared well throughout the post-election vol roll-down and exhibited significantly less volatility of returns relative to outright long delta-hedged straddles (refer above chart).

In support of the long skew (via short OTM puts) lean, at 56% for realized vs. 45% for SABR implied, spot-vol correlation is performing. Though, complicating matters, impact from election will (somehow artificially) remain embedded in realized spot-vol for nearly full 2 more months (in case of 2m trailing).

Mexico-induced reprisal of risk in Brazil best hedged via long 3M USDBRL straddles subsidized by selling OTM puts realized spot-vol for nearly full 2 more months (in case of 2m trailing).

We recommend delta-hedged 3M USDBRL long ATMF straddles @14.35/14.6 indic vs short 25D puts @13.5 choice, in 100:130 notionals. Courtesy: JPM

Currency Strength Index: FxWirePro's hourly USD spot index is inching towards 22 levels (which is bullish), while hourly EUR spot index was at 17 (mildly bullish) while articulating (at 13:24 GMT).

For more details on the index, please refer below weblink: