South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei

BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence

Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data

The Riksbank maintained status quo by leaving key interest rates unchanged as expected but took down the rate path by 5-7bp throughout the forecast horizon (through 2021). The minutes from Riksbank’s monetary policy meeting on 5 September were slightly more hawkish than expected. The majority of the board now sees the first-rate hike at the meeting in December or February.

Most importantly, for the very near term, they ruled out the smaller October hike by explicitly stating that the repo rate will be “raised by 0.25 percentage points either in December or February.” That a lower rate profile (even if in 25bp increments rather than in smaller amounts) was accompanied by a stronger growth forecast (2018 GDP was upgraded from 2.5% to 2.9%; 2019 from 1.9% to 2%) and only modestly lower inflation forecasts for the coming years further shines the spotlight on the ongoing dovish bias from the Riksbank and their single-minded focus on inflation.

Following the Riksbank outcome, we re-initiated tactical SEK shorts intra-week, recall we turned neutral from underweight in July as the meeting opens yet another window for using SEK as a funding currency in the interim with a rate hike not on the horizon till at least December.

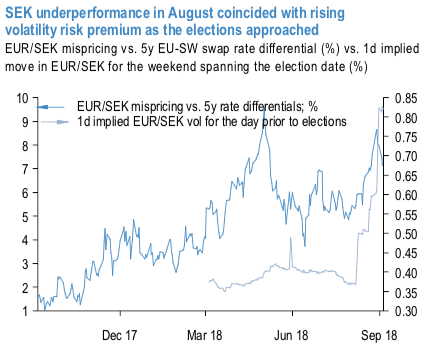

The near-term risk to SEK shorts comes from the general elections over the weekend and the CPI print next Friday, but we expect any gains from these two events to be limited. For markets, the relevant issue in the elections will be the extent to which the Swedish Democrats gain share.

A benign outcome in line with the base case could result in some SEK outperformance as the August weakening in part has coincided with an increase in the risk premium for the election date (refer above chart), but we expect the SEK bounce to be shallow. Similarly, even a firm SEK print on Friday will not necessarily provide enough fodder for SEK bulls with three more CPI prints till the December meeting. Meanwhile, the sensitivity to a softer print is likely to be larger.

Precisely, we advocate outright longs in NOKSEK and long EURSEK through options. Like SEK, we have been noting that NOK is cheap on several metrics as well and focus will now turn now turn to Norges Bank on September 20thwhere the central bank is expected to deliver its first-rate hike since 2011. The combination of cheap valuations and a more activist central bank leads us to re-initiate NOKSEK longs.

We also think that SEK is likely to stay weak vs. EUR although moves will likely be more limited given already stretched valuations.

Hence, we recommend long EURSEK through a call spread financed by a short put to also reflect the view that EURSEK will likely not head materially lower from current levels.

Trade tips:

Buy spot FX NOKSEK at 1.0830. Stop at 1.06.

Buy 2m EURSEK 10.60-10.75 call spread vs short 10.3050 put for 18.6bp. Spot reference: 10.4193. Courtesy: JPM

Currency Strength Index: FxWirePro's hourly EUR spot index is flashing at 51 levels (which is bullish), while hourly USD spot index was at -41 (bearish) while articulating at (11:46 GMT). For more details on the index, please refer below weblink: