S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

Most of the GBP pairs are gaining soon after Boris Johnson’s victory, but getting Brexit done isn’t a reason for GBP to cheer in a long run, not as cliff-edge risks remain. Despite Johnson’s surprisingly large majority, we see no basis to revise our GBP forecasts – these have been unchanged for quite a few months now. We continue to envisage a period of reflection and consolidation as the central issue regarding Brexit remains to be clarified, i.e. the nature of any new Free Trade Agreement between the UK and the EU. The election may have resolved certain uncertainties, a renaissance in UK growth seems to be dubious, while assumptions about massive currency hedges that are set to be unwound are precisely that, assumptions).

We have listed some major driving forces of GBPJPY and advocated suitable hedging strategies.

Bullish GBPJPY Scenarios:

1) The UK government announces a much more stimulatory budget in March (the manifesto envisaged fiscal thrust of 0.4-ppt for 2020 and nothing thereafter).

2) Johnson eventually acknowledges the need for a lengthier transition period.

3) The UK government softens its stance and agrees to closer regulatory alignment to maintain frictionless trade.

4) Momentum in JPY selling flows related to outward portfolio investments and FDI strengthens further.

Bearish GBPJPY Scenarios:

1) The UK economy fails to rebound after the election.

2) The BoE cuts rates in January or March.

3) Johnson refuses to soften his trade stance, leading to an even greater risk of a no deal exit at the end of 2020.

4) Momentum builds for a 2nd referendum on Scottish independence.

5) The UK -EU extends the transition period beyond December.

6) Trade tensions between the US and China intensify and global investors’ risk aversion heightens significantly

Alternatively, ahead of BoJ monetary policy that is scheduled for the next week, with UK PMI numbers, shorting futures of mid-month tenors are advocated with a view of arresting the resumption of major downtrend. Writers in a futures contract are expected to maintain margins in order to open and maintain a short futures position.

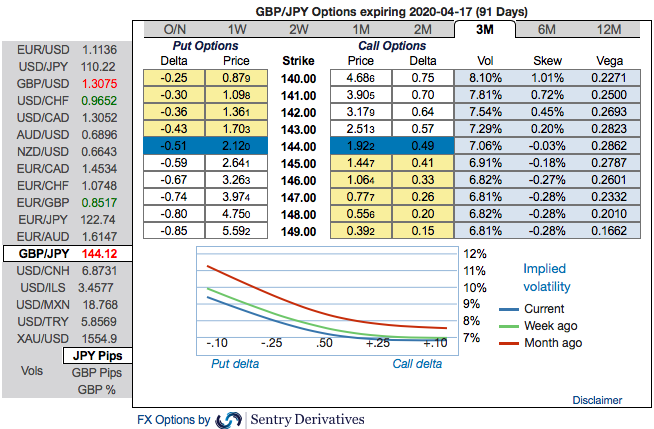

The GBPJPY has been volatile, appreciating to just shy of $144.130 after bottoming out at 140.817 level, the reports of a Brexit deal agreement have also cushioned. Currently, trading with little exhaustiveness, still, it is well up from last week’s lows.

Even so we believe it worthwhile increasing our bearish beta to GBP through re-selling GBPJPY (our single most successful trade to date this year).

OTC outlook and Hedging Strategy: The implied volatility of this pair that display the highest number among entire G7 FX universe.

While the positively skewed IVs of 3m tenors signify the hedgers’ interests to bid OTM put strikes up to 139 levels (refer above nutshell).

Accordingly, put ratio back spreads (PRBS) are advocated on the hedging grounds. Both the speculators and hedgers who are interested in bearish risks are advised to capitalize on current abrupt and momentary price rallies and bidding theta shorts in short run, on the flip side, 3m skews to optimally utilize delta longs.

The execution: Capitalizing on any minor upswings , we advocate shorting 2m (1%) OTM put option (position seems good even if the underlying spot goes either sideways or spikes mildly), simultaneously, go long in 2 lots of delta long in 2m ATM -0.49 delta put options (spot reference: 143.786 levels while articulating).

The position is a spread with limited loss potential, but varying profit potential. The degree of profit relies on the strength and rapidity of price movement. The position uses long and short puts in a ratio, such as 2:1 or 3:2, to maximize returns. Courtesy: Sentry & JPM