Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  BOJ Rate Decision in Focus as Yen, Inflation, and Nikkei Hang in Balance

BOJ Rate Decision in Focus as Yen, Inflation, and Nikkei Hang in Balance  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  DOJ Ends Probe Into Fed Chair Jerome Powell, Boosting Kevin Warsh Confirmation Prospects

DOJ Ends Probe Into Fed Chair Jerome Powell, Boosting Kevin Warsh Confirmation Prospects  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  RBA Raises Interest Rates to 4.35% Amid Rising Inflation Risks and Middle East Tensions

RBA Raises Interest Rates to 4.35% Amid Rising Inflation Risks and Middle East Tensions  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025

Yellen dropped a heavy hint last week that a rate hike was coming on the Ides of March. That too is the day of the Dutch general election, though it remains unlikely that the populist Party for Freedom will secure a majority of parliamentary seats, especially with recent opinion polls indicating waning support.

US 10-year bond yields have traded to the top of this year’s range, and would need to break through to the upside to get the dollar’s momentum going. USD/JPY continues to be highly sensitive to US bond yields. Another decent US payrolls report this Friday should cement the emerging consensus of a March Fed hike.

After a month of relentless pounding, FX option markets are ending February with front-end vols in USD-pairs on a slightly firmer footing, thanks to what looks like a concerted campaign by Fed officials to nudge the market towards pricing in a March hike. That effort is largely successful judging by the climb in OIS-implied probability of a March move to 90%, but we suspect that markets will additionally test the odds of a rise in the 2017 median dot from the current three hikes to four in the run-up to the meeting.

Gamma in dollar pairs is likely to firm over the next two weeks with the Fed narrative returning as a market driver.

Owning USD-gamma in commodity FX funded with shorts in select yen crosses (EURJPY, CHFJPY) is a reasonable RV orientation.

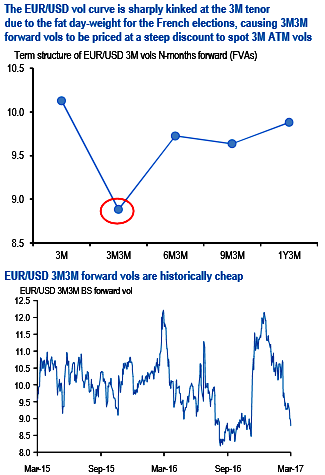

EURUSD 3M3MFVAs are asymmetric French election hedges given their steep discount to event premium-heavy 3M ATM vols and attractive entry levels. -3M/+6M calendar spreads of EUR calls/JPY puts are worth tracking as post-election reflation plays given vol curve inversion beyond 3M expiries.