BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks  Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand

Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand  BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei

BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  RBI Hits Pause as Geopolitical Storm Clouds Gather

RBI Hits Pause as Geopolitical Storm Clouds Gather  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

ECB is scheduled for their monetary policy this week, with the EURUSD continuing to stand above 1.11 ahead of Thursday’s ECB monetary policy meeting, the European central bank is all set to publish details on the allocation of its PEPP programme and focus will be on the potential skew towards Italian and French government bond holdings.

After a number of council members signalled steps of this nature - amongst them the ECB President Christine Lagarde, the market is now expecting the ECB to extent its current asset purchasing programme (PEPP) today. The amount which they would have to extent the programme by, which currently has a target volume of EUR 750bn. to surpass or disappoint market expectations. In the end we do not think that will be relevant for the euro anyway.

As long as sentiment on the market allows, it is going to continue its uptrend anyway. Of course a “hawkish” surprise, i.e. a less aggressive easing of monetary policy, might reinforce the trend briefly.

First of all it would confirm the market in its positive view of economic prospects and secondly many might see it as a sign that the ECB feels less obliged to fight the crisis now that the EU is planning on putting together a generous recovery fund.

What could put a break on the euro’s development though is the fact that much positive economic news has already been priced in - perhaps even too much. Even if the rise in sentiment indicators is no doubt positive this was to be expected after many countries eased their lockdown requirements so that companies could resume production and shops were allowed to open again.

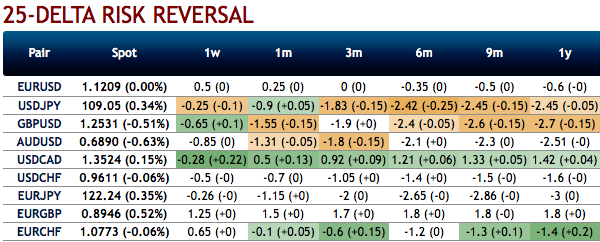

EURUSD risk reversals are trading positively again for tenors below 3-months, and at almost zero for 3-months (refer 1st chart). Because the dollar is less suited as a safe haven? Perhaps marginally. Above all because the market is considering the risk of a second wave of the pandemic to be low and considers a major, risk-driven slide in EURUSD to be less likely. Otherwise butterflies would not be virtually back at pre-corona levels. That might be sensible pricing levels for all those market participants who can spread their risks. Anyone not able to enjoy that luxury might be pleased about this good opportunity to hedge non-diversified risks against a renewed wave of risk aversion.

EUR risk reversals have still been indicating the hedging sentiments for the bearish risks in the long run, as the fresh negative bids are added to the positive RRs for 1-3m tenors.

Most importantly, the positively skewed EURUSD IVs of 3m tenors are stretched on either sides but with slight biasness towards downside hedging risks (refer 2nd chart), while IVs are shrunk below 6.5% across all the tenors.

Hence, considering all these factors, the below options strategies are advocated.

Options Strategy: Contemplating above factors, activated 1m butterfly spread on trading grounds. Initiated longs in 1m OTM -0.49 delta put while simultaneously shorting ATM put with similar expiries and buy 1m OTM 0.5 delta call while simultaneously shorting an ATM call with similar expiries. This strategy is structured for a larger probability of earning a smaller but certain profit as EURUSD is perceived to have a low volatility.Courtesy: Sentry, Saxo & Commerzbank