Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  ECB Signals Possible Interest Rate Move if Inflation Outlook Fails to Improve

ECB Signals Possible Interest Rate Move if Inflation Outlook Fails to Improve  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  BOJ Governor Kazuo Ueda Hints at Rate Hike as Inflation Pressures Build

BOJ Governor Kazuo Ueda Hints at Rate Hike as Inflation Pressures Build  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  OECD Sees Bank of Japan Raising Interest Rates to 2% by 2027

OECD Sees Bank of Japan Raising Interest Rates to 2% by 2027

We have received two surprises to reduce downside risks to USDJPY.

One is from politics and the other is from the macro side:

With respect to politics, we had expected that FX and trade issues would have been discussed at the U.S.–Japan summit held on February 10-11, given the series of fierce attacks on Japan by President Trump before the meeting. Yet, these issues were not discussed while the communique confirmed the two nations are firm allies and the Senkaku islands fall within the scope of Article 5 of the U.S.-Japan Security Treaty. The summit was more than perfect for Japan.

On the macro side, with the chorus of hawkish commentary by the Fed officials, the market has priced in a March hike immediately. Given that, widening U.S.-Japan yield spreads have brought USDJPY higher and the pair is now reaching the upper end of its trading range since mid-January.

We now expect the Fed to deliver three hikes in this year (Mar, Jun, and Sep vs. May and Sep previously).

Driving forces for bullish/bearish scenarios:

USDJPY to 125 if 1) Strong US growth leads more aggressive Fed hikes, 2) Japanese fiscal policy becomes more expansionary, resulting in higher Japan’s inflation expectations.

USDJPY to 100 if 1) The global investors’ risk aversion heightens significantly, 2) Weak US economy dampens hopes for Fed hikes, 3) The U.S. administration talks down USDJPY aggressively.

Potential triggering events:

Econ. Min. Seko meets Ross (Mar 16)

BoJ meeting (Mar 16)

G-20 (Mar 17-18)

USTR report on trade barriers (end-March).

Hedging Framework:

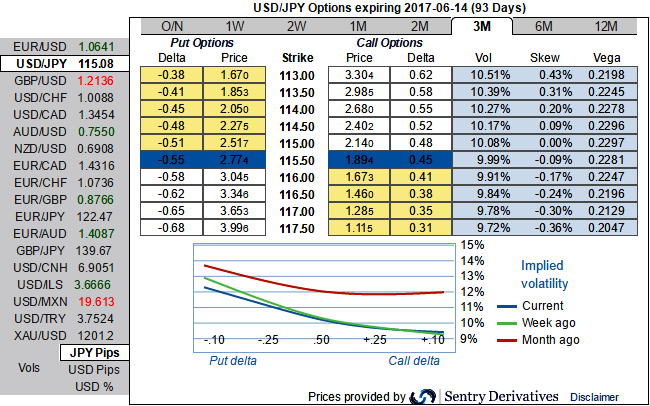

The positively skewed IVs of 3m tenors are indicating the hedgers’ interest in OTM put strikes. With bearish-neutral risk reversal in this tenor, we wouldn't be surprised even if the underlying spot FX evidences the interim spikes ahead of above mentioned Fed hiking cycle, but the below option strategy to optimally arrest any abrupt slumps towards 112.169 and 111.450 levels sooner or later.

Hence, we deploy ITM puts with longer tenors in our option strategy as the delta risk reversals favor bearish targets, hence in order to keep the risks on either side on the check we reckon diagonal debit put spreads are best suitable as the IVs and premiums are reasonable considering daily swings on technical charts.

So, here goes the strategy, Diagonal Debit Put Spread = Go long 3m (1%) ITM -0.49 delta Put + Short 1m (1%) OTM Put with lower Strike Price with net delta should be at around -0.40.

For a net debit, bear put spread reduces the cost of trade by the premium collected (on the shorts of OTM put) and keeps option trader to participate in downward moves and any upswings in abrupt.