Eurozone Recession Risks Rise as Middle East Conflict Threatens Growth, ECB Official Warns

Eurozone Recession Risks Rise as Middle East Conflict Threatens Growth, ECB Official Warns  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  RBA Raises Interest Rates to 4.35% Amid Rising Inflation Risks and Middle East Tensions

RBA Raises Interest Rates to 4.35% Amid Rising Inflation Risks and Middle East Tensions  Bank of Japan Signals Potential Rate Hike as Inflation Risks Rise Amid Energy Shock

Bank of Japan Signals Potential Rate Hike as Inflation Risks Rise Amid Energy Shock  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts

Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts  South Korea Central Bank Signals Cautious Policy Amid Inflation and Middle East Tensions

South Korea Central Bank Signals Cautious Policy Amid Inflation and Middle East Tensions  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  AI-Driven Inflation Raises U.S. Consumer Prices, Goldman Sachs Says

AI-Driven Inflation Raises U.S. Consumer Prices, Goldman Sachs Says  Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing

Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing

The Japanese yen once again continues the appreciation trend seen over the past few days. The reason is a recent rise in speculation that the Bank of Japan (BoJ) might tighten its monetary policy this year. This speculation was further fuelled yesterday by the central bank’s announcement to be buying fewer long-dated government bonds as part of its asset purchasing programme in the future. Both yields and JPY went up significantly as a result.

Since inflation in Japan remains well under the envisaged target, the Bank of Japan (BoJ) is condemned to maintaining its ultra-expansionary monetary policy for the foreseeable future. The fact that the government is continuing with its Abenomics programme also points towards a continued expansionary monetary policy over the coming two years.

We, therefore, expect a weaker yen, in particular, if the US central bank Fed continues to hike interest rates as expected and the ECB slowly tapers its asset purchasing scheme

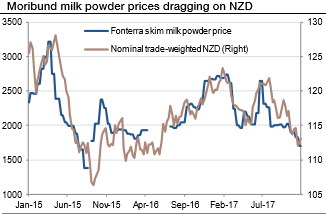

On the flips side, The Kiwi is expected to lose its pole position in terms of offering the highest central bank policy rate in G10 next year, and this should keep the currency a laggard. Moribund milk powder prices should also continue to drag on the currency (refer above graph).

There are therefore cross-currents buffeting the growth outlook next year, but the impact on 1H 2018 is likely to be the net negative. Inflation should consequently remain contained despite the 4.8% rise in minimum wages in April 2018. The government is also reviewing the RBNZ's mandate with the intention of inserting "maximum employment" as a second mandate alongside price stability and moving to a committee structure for monetary policymaking. The RBNZ is therefore expected to stay on the sidelines through 2018 in the face of the institutional changes and countervailing fiscal effects.

OTC Outlook and hedging strategies:

ATM IVs of NZDJPY is trading between 7.14% and 7.91% for 1w and 1m tenors respectively and positively skewed IVs of 1m tenors are evidencing bearish hedging interests. Bids for OTM puts upto 76.50 is noticeable to signify downside risks.

Thus, conservative hedgers can prefer the below strategy:

Debit Put Spread = Go long 1M ATM -0.49 delta Put + Short 1m (1%) OTM Put with lower Strike Price with net delta should be at -0.46. Please be noted that the positive payoff structure would be generated as it keeps dipping below current levels but remain within OT strikes.

For a net debit, bear put spread reduces the cost of trade by the premium collected (on the shorts of OTM put) and keeps option trader to participate in downward moves and any upswings in abrupt.

Moreover, the risk is capped to the extent of initial premium paid, as opposed to unlimited risk when short selling the underlying outright.

However, put options have a limited lifespan. If the underlying FX price does not move below the strike price before the option expiration date, the put option will expire worthless.

Currency Strength Index: FxWirePro's hourly NZD spot index is inching towards 18 levels (which is neutral), while hourly JPY spot index was at 115 (highly bullish) while articulating (at 11:41 GMT). For more details on the index, please refer below weblink:

http://www.fxwirepro.com/currencyindex.

FxWirePro launches Absolute Return Managed Program. For more details, visit: