UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

The news of the additional US tariffs also resulted in EM currencies/equities crumbling overnight. Apart from the Chinese readings, Asian manufacturing PMIs came in mixed to weaker. Short-end EMFX vols are ‘waking up’ again, with Chinese equities slumping in early trade on Friday.

Overall, expect USD-Asia upside to persist, especially with regional currencies now lacking the buffer of net portfolio inflows. Asian (govie and IRS) yields meanwhile may be expected to take the cue from the global core curves and explore the downside once again, flushing out any ambiguity witnessed immediately after the FOMC.

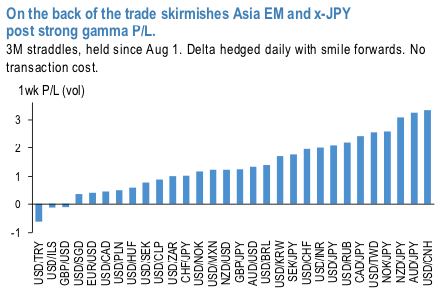

Spot gyrations generated strong gamma returns especially in Asia EM and x-JPY (refer 1st chart). How widespread and how impactful the trade escalation has been the best seen from the 1-week returns which are >90 percentile of YTD weekly returns for 26 out of 30 currencies in the Exhibit. We do not see a quick resolve and remain defensive though the current indications are that PBoC may want to bring back calm into FX.

The PBoC activity on clamping down the CNY day-to-day spot moves over the last few sessions shows that the central bank might be comfortable with the current level of FX weakness. CNY vols came off from the recent multi-year highs, and the 6M is now back to sub-6vol handle. The US-China trade developments remain very fluid and we are bound to see a few more adverse episodes.

Cheap vega ownership: In anticipation of the vega tenors receiving more attention with the spot now under the watchful PBoC hand, we recommend using the favorable vol entry levels to add vega.

Moreover, pricing of the CNH skew offers an attractive setup to own cheap CNH vol exposure directly via 6M 25D USDCNH puts (delta-hedged), i.e. to own the weak (or the "wrong") side of the risk- reversal. The structure provides long vega exposure but at smaller decay costs. The choice of the delta strike (25D to 35D) reflects a trade-off between deriving adequate discount vis-à-vis ATM vols and gamma/vega exposure. Based on the historical P/L time series in 2nd chart the "wrong" side OTM vega has been an efficient proxy for the CNH ATM straddles during adverse episodes.

Consider: 6M or 9M USDCNH 25 delta puts @5.4/5.725 indic for 6M and @ 5.375/5.675 indic for 9M, delta hedged. Courtesy: JPM