Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX  FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022

The stakes are high this week. A big shift in the trajectory of inflation in Australia would threaten both our view that the market will not move to price in hikes into the OIS strip, and that the AUD remains capped, with a range top at USD0.7850.

However, this is not our core view. A number of factors (rising under-employment, retail sector competition, and soft rental markets) all continue to suggest that we have not reached a significant point of inflection for core inflation. As such, the strategy into the number is to sell any strength in the AUD or any attempts to price in a tightening track for the RBA.

OTC updates & hedging strategy:

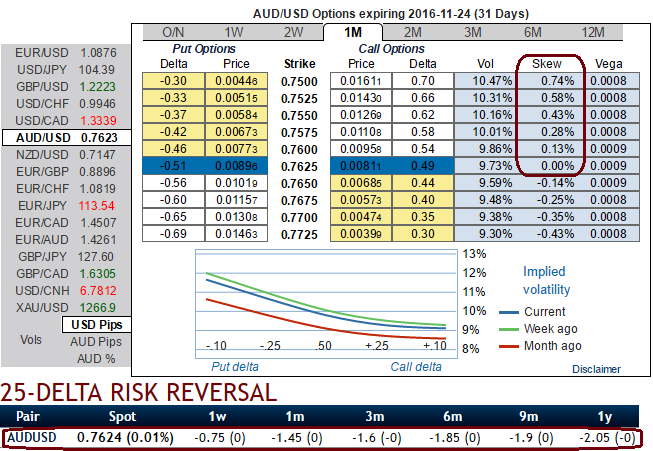

Please be noted that the implied volatility for near month at the money contracts of this APAC pair has been dropped below 9.75% for 1m expiry but IV skews emphasize the interest of OTM put strikes.

Simultaneously, the delta risk reversal across various tenors divulge more interests in hedging activities for downside risks.

As a result, we can understand ATM puts have been costlier where the spot FX market direction of this pair is heading towards 0.7628 levels. So, the speculators and hedgers for bearish risks are advised to optimally utilize the upswings and bid on 1m IV skewness and risks reversal indications.

The OTC options market appeared to be more balanced on the direction for the pair over the 1-3m time horizon and as a result delta risk reversal for AUDUSD has been maintaining negative which means puts are in higher demand and overpriced comparatively.

Hence, AUDUSD's lower IV with negative delta risk reversal can be interpreted as the market reckons the price has downside potential for large movement in the days to come which is resulting option writers on competitive advantage and making derivatives instruments for downside risks have been overpriced and fresh shorts are more on the cards.

Well, contemplating the above risk reversal computations, we construct strategy comprising of both calls as well as puts in the ratio of 3:1 so as to suit the swings on either directions.

Here goes the strategy, go short in 1m OTM calls and simultaneously, 3 lots of 3m puts (+1% ITM, ATM and +1% OTM strikes) are preferred to suit the prevailing losing streaks. So thereby the combination would be executed for net debit and the cost is reduced by short side.

Moreover, the strategy could be counterproductive as the skews in 1m IVs favors OTM puts strikes.