BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei

BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei  ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns  Asian Currencies Slip as Dollar Holds Firm, Yen Near Four-Decade Low Ahead of Fed, Jobs Data

Asian Currencies Slip as Dollar Holds Firm, Yen Near Four-Decade Low Ahead of Fed, Jobs Data  Asian Currencies Stay Range-Bound as Investors Eye China Data, RBNZ Outlook and U.S.-Iran Ceasefire

Asian Currencies Stay Range-Bound as Investors Eye China Data, RBNZ Outlook and U.S.-Iran Ceasefire  RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists

RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Trump Urges Gasoline Retailers to Cut Prices to $2.50 Per Gallon, Warns of Legal Action

Trump Urges Gasoline Retailers to Cut Prices to $2.50 Per Gallon, Warns of Legal Action  Asian Stocks End Strong Quarter as Dollar Surges, Yen Hits 40-Year Low Ahead of US Jobs Data

Asian Stocks End Strong Quarter as Dollar Surges, Yen Hits 40-Year Low Ahead of US Jobs Data  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  UK House Prices Hold Steady in June as Annual Growth Misses Forecasts

UK House Prices Hold Steady in June as Annual Growth Misses Forecasts  Dollar Slips Ahead of Key U.S. Jobs Data as Fed Rate Outlook, ECB, and Iran Talks Shape Forex Markets

Dollar Slips Ahead of Key U.S. Jobs Data as Fed Rate Outlook, ECB, and Iran Talks Shape Forex Markets  BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

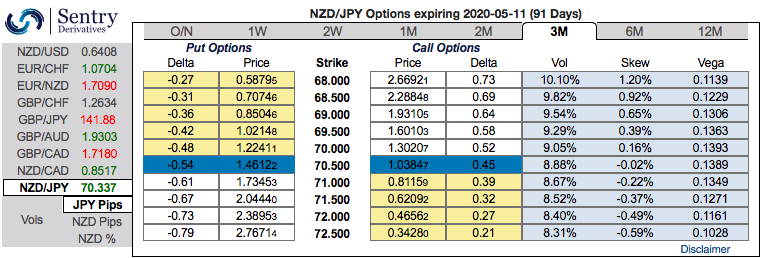

RBNZ’s monetary policy that is scheduled for Wednesday. The kiwis central bank cut 50 bps in its August meeting and had said that there was room to cut further "if required." We interpret this as an easing bias rather than a signal. In other words, the RBNZ views a cut as more likely than a hike, but is not committing to either at this point. We reckon that the prevailing rallies of NZDJPY are momentary, NZD is expected to depreciate towards 67 levels by year-end.

Although NZDJPY shows interim rallies upon hammer and dragonfly doji patterns 70.229 and 70.157 levels respectively, these upswings seem momentary as the overbought pressures The decline in January could extend below 70.00 if the coronavirus epidemic persists.

Event risk during this week comes from wage data and a leading index. Although we have a positive outlook for the NZ economy in 2020, the global risks are expected to persist.

Hence, it is wise to capitalize on interim rallies and optimize ‘debit put spreads’ ahead of the central bank’s policy event. Before we deep dive into the hedging framework, better to be aware of bearish driving forces of NZDJPY.

Bearish NZDJPY scenarios:

1) Tightening by banks forces a deeper slowdown in credit growth, and weakens the agricultural sector;

2) The immigration rolls over more quickly.

3) The global investors’ risk aversion heightens significantly;

4) Global economy enters serious recession; and middle-east tensions escalate sharply.

OTC Updates, Trade and Hedging Recommendations:

The positively skewed NZDJPY IVs of 3m tenors signify the downside risks, the bids for OTM put strikes up to 68 levels clearly indicates hedgers are inclined for further downside risks (refer above nutshells evidencing IV skews). The major downtrend continuation shouldn’t be panicked the broad-based bearish outlook amid minor rallies.

Hence, it is conducive for OTM put writers capitalizing on short-term rallies so as to reduce long-leg meant for downside hedging.

The execution of strategy goes this way: Initiate longs in at the money -0.49 delta put options of 3m tenors, simultaneously, short (1%) out of the money put options of the narrowed expiry (preferably 2w tenors), the strategy is executed at net debit (activated when spot reference: 70.957 levels).

Well, a higher (absolute) Delta value is desirable on long leg in the above stated strategy. Whereas, the Theta is positive on short leg; as the time decay is good for an option writer (that’s why we’ve chosen narrowed expiry). The short side likely to reduce cost of hedging with time decay advantage on short leg, while delta longs likely to arrest potential bearish risks.

Alternatively, shorts in the mid-month futures have been advocated with a view of arresting further downside risks. Courtesy: Sentry