BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey  Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand

Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

BoE governor Mark Carney is scheduled to deliver a speech, usually, as head of the central bank, which controls short-term interest rates, he has more influence over the nation's currency value than any other person. Traders scrutinize his public engagements as they are often used to drop subtle clues regarding future monetary policy.

In the recent past, he has warned that new financial technology could damage the business model of traditional banks as savers turn away from mainstream lenders.

Well, JP Morgan has recently upgraded 2017 GDP growth forecasts but continue to expect a slowdown during the year.

While scope for some more hawkish rhetoric from the BoE, but expectation that the majority to hold rates this year.

Some limited payback expected in March inflation.

This week we revised up our 2017 growth forecast to reflect a more positive European growth backdrop and a slower-than-expected loss of momentum in some of the business output surveys in 1Q. Although some of the more hawkish MPC members may dissent this year, we expect the majority to stay patient on rates in anticipation of weakening consumer spending growth.

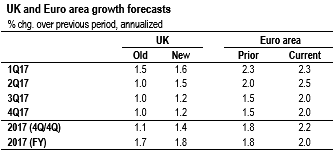

Our growth revisions raise our full-year 2017 GDP growth projection by 0.2%-pt to 1.9%. And the average quarterly annualized pace has risen by 0.3%-pt, from 1.1% to 1.4% (refer above table). The upgrade is larger in 1H17 (0.4%) and reflects some surveys’ greater than expected resilience, including in this week’s March services PMI. The upgrade to 2H17 is smaller (0.2%) and reflects the changes we made last week to our Euro area growth forecast.

Despite these revisions, our 2017 full-year growth forecast remains slightly below the BoE’s 2.0% forecast. The larger forecast change for the BoE at next month’s Inflation Report likely will be to inflation, where we expect it to raise its existing 4.2% 2017 CPI forecast closer to our current 2.7% projection.

Together with the stronger global outlook, this could encourage some of the shy hawks on the MPC to vote for higher rates at the upcoming May meeting. But we continue to expect the majority to have an eye on the weak path for real incomes this year, and signs from the latest data that a consumer slowdown already is under way. As a result, most on the MPC should resist the temptation to support higher rates, at least until it becomes clearer how the consumer is responding to the purchasing power squeeze.

Recent MPC commentary appears to support this view. Although Vlieghe is the most dovish on the MPC, his comments in a speech this week highlight a cautious stance on rates due to concerns about the consumer, and limited policy easing options available to the MPC in the event of a more significant slowdown. Even relatively hawkish McCafferty sounded concerned about the consumer this year in comments last week.