2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  ECB Rate Outlook: Ceasefire Eases Pressure but Hikes Still Expected in 2026

ECB Rate Outlook: Ceasefire Eases Pressure but Hikes Still Expected in 2026  Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts

Fed’s Goolsbee Warns Inflation Remains Elevated, Signals Caution on Rate Cuts  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

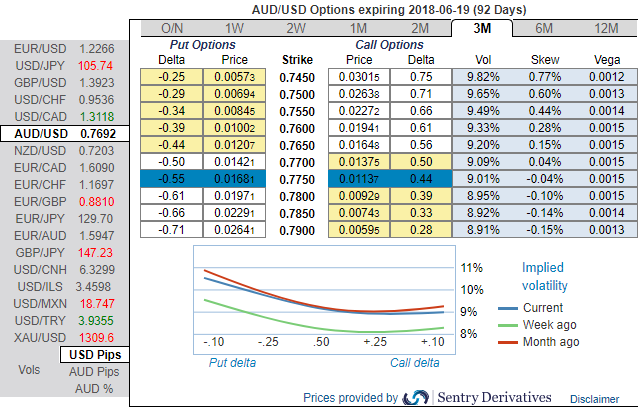

AUDUSD near-term momentum appears to be negative, targeting the 0.7650-0.7700 area if the USD rebound persists.

While the medium-term perspective remains slightly pricey compared to short-term fair value projections, as yield differentials along the curve move steadily in the US dollar’s favor.

This weight on AUD should only increase over the next year or two. Shorter-term though, markets are already priced for a Fed hike this month and no change from the RBA for many months.

Moreover, commodity prices have emerged from Asia’s Lunar New Year holidays still holding most of the late 2017 gains.

Optimism over global growth remains intact though US-driven trade tensions pose downside risks to global trade volumes and AUD. We look for 0.78 end-Mar and 0.74 end-Q2’2018.

OTC outlook and hedging perspectives:

While using rising IVs of longer tenors coupled with the negative shifts adding to bearish risk reversal numbers could be interpreted as an opportunity to deploy longs in OTM puts with theta shorts in ITM put on time decay advantage as the spot FX market reckons the price has downside potential for large movement in the days to come which is resulting option holders’ on competitive advantage.

Without disregarding the Fed’s rate hiking cycle in 2018, the bearish stance of the pair has been substantiated by mounting bearish risk reversals and positively skewed IVs of 3m tenors which is an opportunity for put longs in long-term as the US central bank likely to raise the Funds rates by 25 bps.

Accordingly, we had advocated put ratio back spreads a couple of days ago, wherein short leg is functioning as the underlying spot FX keeps spiking.

Both the speculators and hedgers for bearish risks are advised to capitalize on the prevailing price rallies by bidding 3m theta shorts, 3m risks reversals to optimally utilize Vega longs.

On hedging grounds, fresh Vega longs for long-term hedging, more number of longs comprising of OTM instruments and ITM shorts in short-term would optimize the strategy.

So, the execution of hedging positions goes this way:

Short 3m (1%) ITM put option, simultaneously, go long in 2 lots of vega long in 3m (1%) OTM -0.39 delta put options. A move towards the ATM territory increases the Vega, Gamma, and Delta which boosts premium.

Thereby, the above positions address both upswings that are prevailing in short run and bearish risks in long run by vega longs.

Precisely from the above payoff graph, we can comprehend –

- If underlying spot FX slides down, then the profits are unlimited (refer positive shift in payoff structure).

- Well, there is only one breakeven point at 0.7423 levels.

- The spot FX point at which highest loss occurs is at 0.7619 levels.

- If spot FX markets spike up, then the yields would be limited.

Currency Strength Index: FxWirePro's hourly AUD spot index is inching towards -114 levels (which is highly bearish), while hourly USD spot index was at a tad below 31 (mildly bullish) while articulating (at 07:22 GMT). For more details on the index, please refer below weblink:

http://www.fxwirepro.com/currencyindex.

FxWirePro launches Absolute Return Managed Program. For more details, visit: