Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

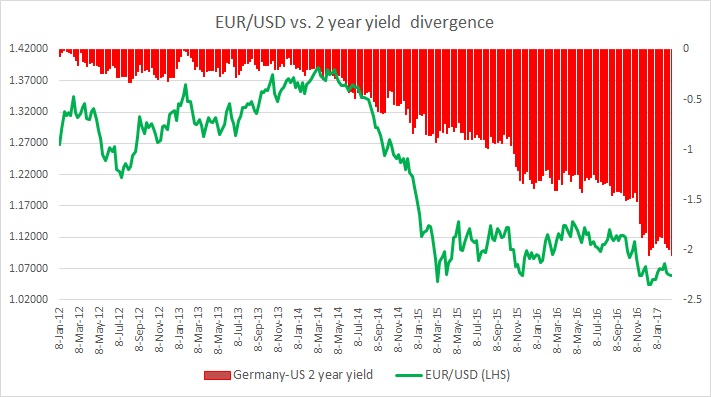

The chart above shows, how the relationship between EUR/USD and 2-year yield divergence has unfolded since 2012. It is evident that these short rates have been a key influencing factor for the pair as policy divergence became evident since 2013.

Past divergence and move in the exchange rate:

- As the speculations from extraordinary monetary stimulus became frenzy since the beginning of 2014, yield divergence between German 2 year bond (considered as European benchmark) and the US 2 year note went from -0.18 percent at the beginning of 2014 to -0.78 percent by the end of the year and EUR/USD declined from 1.367 to 1.2 by year end.

- We saw further drop in the EUR/USD exchange rate in 2015 as ECB introduced monetary stimulus but the yield failed to follow that fast, it only started declining as expectations over further stimulus grew and by end of December more than 50 basis points compared to first quarter of 2015.

- European Central Bank (ECB), however, disappointed in December and only to deliver in March 2016. Since December, Germany-US yield divergence has moved in a range lacking clear direction as Fed became more cautious than expected. So has the EUR/USD.

- From summer this year, the yield spread has started declining again and after Donald Trump won the US presidency, the spread has widened sharply. In August, the spread was at 1.35 percent and it deteriorated to -1.43 percent just before the US election and in December it reached -1.87 percent. Similarly, the euro has declined from 1.11 against the dollar, prior to the election to 1.065.

Since our last evaluation in December, the yield spread has widened further by almost 20 basis points. However, the exchange rate hasn’t followed through, which means there is an intermediate divergence building up. The uncertainties surrounding the upcoming elections in Europe and with regard to the policies in the US are asserting high levels of influence over the exchange rate.

We suspect a further decline in both as the two central banks are clearly on a divergent path.