Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX  FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

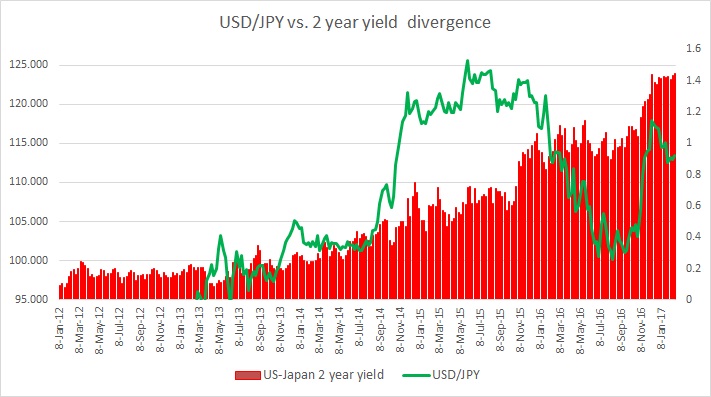

This one pair has been at odds with yield divergence throughout 2016 as the yen benefited from risk aversion and due to market participants’ doubts on BoJ’s abilities to ease policies further. It had shown excellent response to the yield divergence in the past, especially after Bank of Japan (BoJ) announced its quantitative easing program back in 2012. The close relationship lasted until summer of 2015. US-Japan 2 year yield spread rose from 0.13 percent in 2012 to 0.72 percent by May 2015 and hovered there till October and the exchange rate reached from 76 to 126 in that same period.

However, trouble started surfacing after summer. We guess it was triggered by surprise devaluation of the yuan by the Chinese central bank, People’s Bank of China (PBoC).

The yield spread kept rising in favor of the dollar. The yield spread rose more than 30 basis point since summer, but, the yen has strengthened from 126 to as low as 98.

After Donald Trump, the Republican candidate secured a victory in this year’s US election the exchange rate has started to respond to the yield difference once more. After Mr. Trump’s victory, the yield gap jumped suddenly by more than 25 basis points and the yen has weakened to 114 per dollar from as high as 101 per dollar.

Since our last evaluation in December last year, the yield spread has widened by 13 basis points but that has failed to weaken the yen against the dollar as the safe haven currency has once again started benefiting from risk aversion. We suspect the recent spike in inflation worldwide would also lead to speculations of a policy wind up from the central bank and keep the yen relatively higher.