Eurozone Recession Risks Rise as Middle East Conflict Threatens Growth, ECB Official Warns

Eurozone Recession Risks Rise as Middle East Conflict Threatens Growth, ECB Official Warns  BOJ Holds Interest Rates at 0.75% as Policymakers Signal Growing Inflation Concerns

BOJ Holds Interest Rates at 0.75% as Policymakers Signal Growing Inflation Concerns  Japan Inflation Expectations Rise as BOJ Rate Hike Timing Faces Uncertainty

Japan Inflation Expectations Rise as BOJ Rate Hike Timing Faces Uncertainty  RBA Raises Interest Rates to 4.35% Amid Rising Inflation Risks and Middle East Tensions

RBA Raises Interest Rates to 4.35% Amid Rising Inflation Risks and Middle East Tensions  RBA Rate Hike Outlook: Impact on AUD/USD and ASX 200

RBA Rate Hike Outlook: Impact on AUD/USD and ASX 200  DOJ Ends Probe Into Fed Chair Jerome Powell, Boosting Kevin Warsh Confirmation Prospects

DOJ Ends Probe Into Fed Chair Jerome Powell, Boosting Kevin Warsh Confirmation Prospects  Bank of Korea Signals Potential Interest Rate Hikes as Inflation Remains Elevated

Bank of Korea Signals Potential Interest Rate Hikes as Inflation Remains Elevated

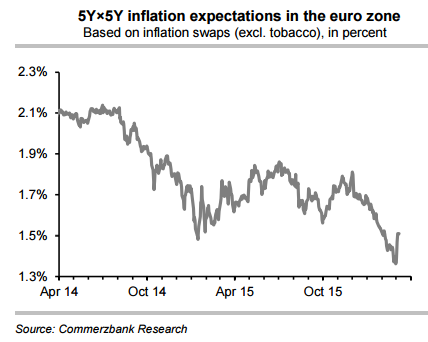

Euroarea headline inflation in February slipped back into negative territory, came in at -0.2% from +0.5% in January. Core inflation unexpectedly plunged 0.3pp to +0.7%, just above the all-time low (+0.6%) reached in January 2015. Since the December meeting, eurozone economic outlook and inflation have weakened, leading indicators have fallen short of expectations. More easing from the ECB on 10 March looks virtually certain. Draghi may not want to repeat the disappointment that took place after the December meeting.

At the March 10th meeting, ECB is expected to lower projections for growth and inflation slightly for the coming years. President Draghi is expected to stress that the ECB's revised inflation profile is surrounded by downside risks since the recent drops in headline and core inflation will likely not be incorporated in the updated projected outlook due to cut-off date reasons.

"The ECB to revise down its 2016 and 2017 inflation forecasts from +1.0% and +1.6% projected in December to +0.4% and +1.4%, respectively. This compares with our revised forecast that inflation is likely to average +0.1% this year and +1.0% next", says Barclays in a research report.

The likelihood of a two-tier system has recently increased from the comments by ECB speakers and the recent increase in lending rates in some countries. The ECB may loosen or remove the deposit rate floor constraint on the purchases in the public sector purchase programme (PSPP) and further broaden the universe of eligible assets than to remove the capital key or bond specific limits.

"News about ECB deliberations ahead of the policy meeting next week indicate growing concern about pushing rates further into negative territory. The focus might be shifting to asset purchases and implementing a tiered deposit rate on excess reserves. This could just be trying to rearrange the deck chairs, as the impact of unconventional policies fade." notes Societe Generale in a report.

Recent indicators suggest that the current modest economic recovery remains driven by domestic demand. February passenger car registrations recorded double-digit annual growth in Germany (+12.1%), France (+13.0%), Italy (+27.3%) and Spain (+12.6%). Euro area retail sales also came in on the strong side in January, beating expectations and advancing for the third consecutive month. Moreover, the latest labour market data for January were reassuring about the euro area private consumption outlook.

"While the outlook for private consumption appears solid, the long-awaited investment rebound may continue to lag, implying downside risks to our expectation that growth will improve +1.6% this year and 1.8% next", adds Barclays.

EUR/USD was trading weaker on the day at around 1.0952 at 1000 GMT, while EUR/GBP was at 0.7740.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

ECB to lower projections for growth and inflation at March 10th meet and take further action

Monday, March 7, 2016 10:18 AM UTC

Editor's Picks

- Market Data

Most Popular