DOJ Ends Probe Into Fed Chair Jerome Powell, Boosting Kevin Warsh Confirmation Prospects

DOJ Ends Probe Into Fed Chair Jerome Powell, Boosting Kevin Warsh Confirmation Prospects  ECB Signals Possible Interest Rate Move if Inflation Outlook Fails to Improve

ECB Signals Possible Interest Rate Move if Inflation Outlook Fails to Improve  Eurozone Recession Risks Rise as Middle East Conflict Threatens Growth, ECB Official Warns

Eurozone Recession Risks Rise as Middle East Conflict Threatens Growth, ECB Official Warns  Bank of Japan Signals Potential Rate Hike as Inflation Risks Rise Amid Energy Shock

Bank of Japan Signals Potential Rate Hike as Inflation Risks Rise Amid Energy Shock

In the past few months, global economic uncertainty has put downward pressure on the price of Canada's resources, weighing on the nation's already beleaguered resource patch.

The price of WTI oil is $45/bbl (as this goes to print), roughly $15/bbl below the July MPR assumption. Thus, the Bank of Canada's (BoC) hopes for in-quarter growth of around 2.8% annualized in 2016 may be difficult to achieve, leaving a wide and persistent negative output gap.

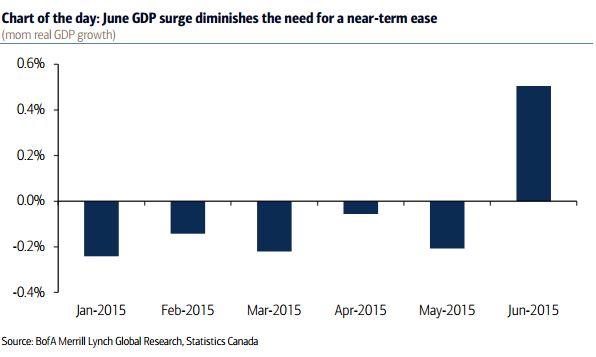

A few weeks ago, a September ease looked somewhat likely. However, oil prices have crept higher, and global headline growth risk has faded. Most importantly, recent news from Canadian economy has been encouraging, with GDP growth in Q2 of -0.5%, in line with the BoC's expectations. June GDP rose by a whopping 0.5% m/m, pointing to a solid end to a very weak first half of the year (Chart of the day). Thus, even, with underlying economic weakness likely on the horizon, there is little reason for the BoC to jump the gun and ease the overnight rate in September.

The BoC will likely nudge the overnight rate down in October if oil prices remain subdued and growth remains tepid, as further stimulus would be needed eliminate economic slack. Although the BoC will likely cite signs that growth is progressing in line with their expectations, global growth uncertainty and downward commodity price pressure should be cited as potential risks. As a mild offset, the CAD depreciation, which in part may have supported by a healthy increase in non-energy export volumes should be cited as a benefit. But the tone on these two offsetting forces should be neutral as it's still too early to tell the ultimate fallout.