US Stock Futures Hold Steady Ahead of June Jobs Report as Fed Rate Outlook Remains in Focus

US Stock Futures Hold Steady Ahead of June Jobs Report as Fed Rate Outlook Remains in Focus  RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists

RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists  UK House Prices Hold Steady in June as Annual Growth Misses Forecasts

UK House Prices Hold Steady in June as Annual Growth Misses Forecasts  US Dollar Rises as Fed Rate Outlook Stays Hawkish, Euro Slips and Yen Near 40-Year Low

US Dollar Rises as Fed Rate Outlook Stays Hawkish, Euro Slips and Yen Near 40-Year Low  Asian Currencies Stay Under Pressure as Dollar Holds Near 13-Month High Ahead of U.S. Jobs Report

Asian Currencies Stay Under Pressure as Dollar Holds Near 13-Month High Ahead of U.S. Jobs Report  FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  Chip Stocks Rally as Samsung and SK Hynix’s $1.3 Trillion Investment Plan Boosts AI Optimism

Chip Stocks Rally as Samsung and SK Hynix’s $1.3 Trillion Investment Plan Boosts AI Optimism

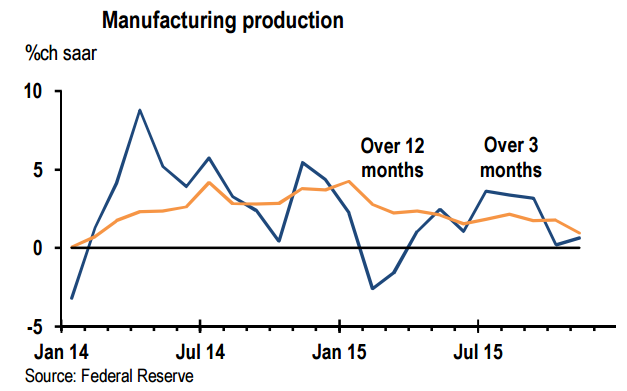

The November IP report confirmed that manufacturing continues to underperform the overall economy. Total manufacturing output was flat in November and non-auto output increased 0.1% samr. This leaves total manufacturing up only 0.8% saar so far in 4Q15 and non-auto manufacturing up 1.1%. These anemic quarterly growth rates are close to the trend in output growth over the first 11 months of the year, 1.1% saar for all manufacturing and 0.6% for non-auto manufacturing.

Moreover, December manufacturing surveys to date point to continued weakness through the end of the year. The PMI had been holding up better than other surveys, but the flash PMI for December dropped to 51.3, its lowest reading since October 2012. The key new orders component dropped to 50.5, its lowest reading since September 2009. Results from the first regional Fed surveys for December were also generally downbeat, in line with the tone of the PMI.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

US manufacturing still struggling

Monday, December 21, 2015 11:39 PM UTC

Editor's Picks

- Market Data

Most Popular