Asian Stocks Rebound as Tech Shares Rally on Fed Rate Cut Hopes and Easing Iran Tensions

Asian Stocks Rebound as Tech Shares Rally on Fed Rate Cut Hopes and Easing Iran Tensions  AI can be a personal trainer in your pocket – but is it safe?

AI can be a personal trainer in your pocket – but is it safe?  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  Turkey Vehicle Sales Fall 11.4% in June as Auto Market Weakens

Turkey Vehicle Sales Fall 11.4% in June as Auto Market Weakens  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  US Resumes Dollar Shipments to Iraq After Months-Long Suspension

US Resumes Dollar Shipments to Iraq After Months-Long Suspension  Trump Administration Declines USMCA Renewal, Opens Talks on New Trade Changes

Trump Administration Declines USMCA Renewal, Opens Talks on New Trade Changes  Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt

Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt  Gold Price Holds Above $4,000 as Fed Rate Hike Expectations and U.S. Jobs Data Weigh on Market

Gold Price Holds Above $4,000 as Fed Rate Hike Expectations and U.S. Jobs Data Weigh on Market  Oil Prices Slip as Iran Talks and Strong Supply Outlook Ease Market Concerns

Oil Prices Slip as Iran Talks and Strong Supply Outlook Ease Market Concerns  BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

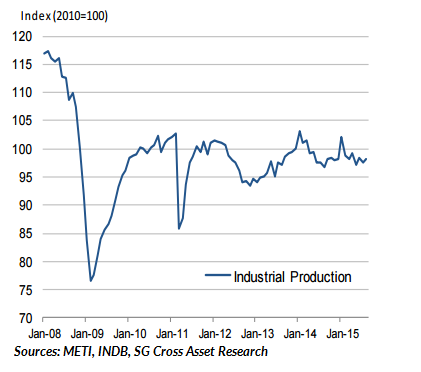

Japan's industrial production data is due for release on Oct 29, Thursday, a day before BOJ policy meeting, at which the c.bank mulls further stimulus. The production data is of great significance as a gauge on whether the BOJ will ease further. Analysts expect industrial production to show a 0.6 percent decline from August, when it dropped a revised 1.2 percent. A gain of 5 percent in September would be needed for third-quarter output to reach zero percent, according to the trade ministry.

"The September industrial production to fall by 0.5% mom, after a decline of 1.2% mom (-0.4% yoy) in August", notes Societe Generale.

Industrial production is more closely correlated with export volumes and the data in September suggest a downside risk to production. In the October Monthly Economic Report by Cabinet Office, the government's assessment on exports and production were both explained as showing "a weak tone recently". Weaker data would fuel concerns that Japan's economy contracted last quarter and entered the second recession since Prime Minister Shinzo Abe took office.

"There will be no surprise if we see a negative number for July-September GDP," Hiroaki Muto, chief economist at Tokai Tokyo Research Center Co. in Tokyo, said after the retail sales report was released.

When the BoJ implemented additional QQE measures in October 2014, production were showing negative growth for two consecutive quarters. If September production is as weak as most analysts anticipate, it will be the third consecutive month of negative growth, confirming its weakness as a trend. Once the September production figure confirms that the production trend is weak, the BoJ is expected to implement additional QQE measures at the 30 October meeting.

Although instability still prevails in emerging economies and the global market, there is a significant possibility that production will ultimately recover. Recovery, however, depends on how strongly exports pick up on the back of a US economic recovery, and also on the extent to which the Chinese economy will avoid an economic downturn. As long as the government and the BoJ keep the policy stance firm, movement towards a complete exit from deflation is intact.

USD/JPY range-bound on the day as nervousness creeps into markets ahead of the much awaited Fed policy decision. Downside remains cushioned as the yen remains weighed down by the dismal retail sales figures. At 1100 GMT Yen was trading at 120.31 against the Greenback, while against the Euro it was at 133.10.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Japan's industrial production to offer cues on BOJ stimulus

Wednesday, October 28, 2015 11:22 AM UTC

Editor's Picks

- Market Data

Most Popular