Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

Bracing USD demand/positive UST yields seemed to restrain any further up-move.

Gold seesawed between tepid gains/minor losses through the early European session and was seen consolidating overnight strong gains to over one-week tops.

The effects of the latter on the FX market, on the other hand, are more difficult. Is there a risk of USD appreciation witnessed since mid-April collapsing now that Trump is considering possible tariffs for car (part) imports into the US? The answer is No.

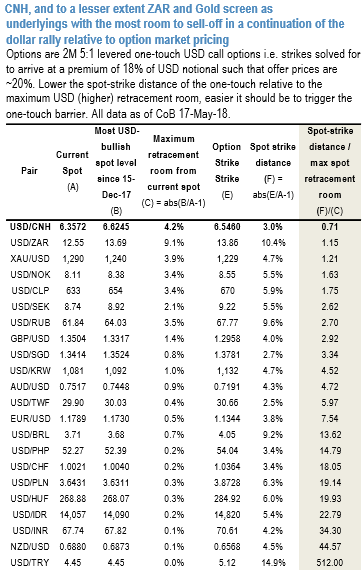

Find the best value in USD calls, judging from the number of queries on the topic recently, real money investors are increasingly beginning to devote option premium to hedge against a continuation of the dollar rally.

On this front, the above nutshell demonstrates a simple relative value screen for short-dated one-touch (OT) USD call options that provide highly leveraged exposure to dollar strength. The rich/cheap measure for directional (not delta-hedged) options used in the table is the ratio of spot-strike distance of 2M 5X geared (i.e. 20% price) OTs deflated by the maximum retracement headroom for the dollar since the onset of the USD downtrend in mid-December; smaller the ratio, less the heavy lifting required of spot to trigger the maximum option payout.

Gold is another interesting underlying to consider dollar longs in. The JPM macro view on the yellow metal remains bullish, but technicals are a key risk as the break below 200D MA could bring further liquidation of spec length.

Front-end risk-reversals in gold have narrowed recently but are still bid for calls, suggesting a degree of complacency/stale positioning that could yet be unwound should dollar strength continue.

At the end of April, the dollar definitively broke out of a narrow range established since mid-January. The move higher in the 10-year Treasury yield was chiefly cited as the driver for the 2% move higher in the broad dollar index. The dollar’s resurgence since April 18 synced with the surge in yields but also the 2% drop in spot gold prices. This sequence of events would normally be considered mundane were it not for the fact that the typical persistently-negative relationship between yields (both nominal and real, short-term and intermediate), and the gold price has broken down since last October.

It is still early days and debatable whether the period of decorrelation has ended. Given that our FX strategists maintain forecasts for a weaker USD over the next couple of quarters, we prefer to keep our long gold trade recommendation in place for now.

Additionally, short-dated gold vols are priced near all-time lows, are one of the most depressed on a cross-asset basis, and are better owned relative to longer-dated vols along a steeply upward sloping curve, hence, there is genuine value in 1M-3M option bets on tactical price declines.

Initiated longs in CME gold for Dec’18 delivery at $1,352.80/oz in February 2018. Subsequently, added an equivalent unit at $1,327/oz in March as well for a new entry level of $1,339.90/oz. Trade target is $1,540/oz with a stop at $1,273/oz. Courtesy: JPM

FxWirePro launches Absolute Return Managed Program. For more details, visit: