China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists

RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

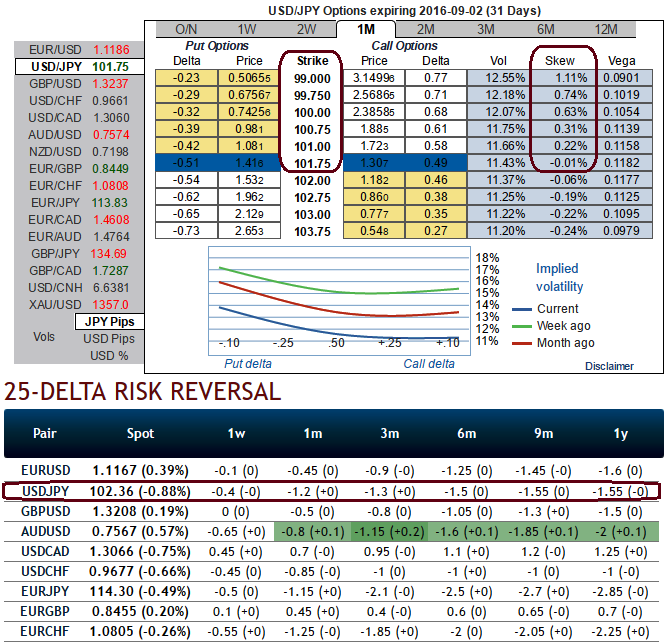

Wise to note that 1M USDJPY ATMs fell from 15.0 pre-meeting to 11.5, significantly undershooting the 1-day forward vol prediction (11.85) despite a 1.5% spot decline on the day, which ought to have provided a modicum of support for vols.

Yen IVs: Live September meeting should keep 2M vol supported; while yen 1-3m risk-reversals still a better sale. Please be noted that the 1m IV skews are more biased towards OTM put strikes, significant changes can indicate a change in market expectations for the future direction in the underlying forex spot rate and these risk reversals evidences the difference in volatility, and therefore price, between puts and calls on the most liquid out-of-the-money (OTM) options quoted on the OTC market.

Even less event-sensitive longer-dated vol sold off hard (3M -1.3, 1Y -1.55), possibly indicating the market’s long vol pre-positioning going into the event that the (non) event proved to be unjustified.

There was also a valuation issue at play, in that yen vols had lagged the sharp collapse in VXY prior to BoJ – held up in all likelihood by the outside chance of a policy regime shift in Japan –and were ripe for a sell-off if the meeting proved uneventful.

The key takeaway from this week’s BoJ is that the September meeting is ‘live’and will feature another will they or won't-they redux, hence ought to command a good amount of event risk premium, perhaps even comparable to the July meeting. If we are right, 2M options spanning the September BoJ should trade at a premium to surrounding points on the curve.

The yen term structure has already repriced to reflect this event bias –2M ATM vols trade 0.6 % pts. over 1M and 3M ATMs – but 3W-4W vols still trade almost at par with 2M.

This presents a theta-efficient opportunity to tactically play for higher USD/JPY into the September BoJ via short 3W vs. long 4W USD calls/JPY puts (e.g. 105 strikes). The tail risk of regime shift in September also means that short yen and cross-yen risk reversals the correct risk-reward trade.