U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  ECB’s Cipollone Backs Digital Euro as Europe Pushes for Payment System Independence

ECB’s Cipollone Backs Digital Euro as Europe Pushes for Payment System Independence  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  South Africa Eyes ECB Repo Lines as Inflation Eases and Rate Cuts Loom

South Africa Eyes ECB Repo Lines as Inflation Eases and Rate Cuts Loom  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

The current price action in the euro remains choppy but essentially range-bound. The trade-weighted index gained 2.5% in the month to mid-September on what seemed like a re-think of the euro’s exposure to Turkey, but then gave back around 1.5% over the past few weeks as Italian stress came to the fore and the dollar was buoyed by the re-think of Fed policy. Over the past 24 hours the euro has turned higher once again as equities have slumped as this has caused a de-risking of the (small) short EUR positions the spec market had established over Italy.

Looking through the month-to-month gyrations we are holding our forecasts steady this month. The end- 2018 projection for EURUSD is modestly lower (1.130) and predicated on a combination of 1) continued divergence in near-term macro-economic momentum between the US and the Euro area and 2) probable further tensions over Italy’s budget if, as seems likely, this is rejected by the EU Commission. The possibility that the BTP spread could overshoot towards 400bp and in turn de-stabilise banks justifies downgrading the risk bias around this forecast from bullish to neutral.

Beyond that, we continue to expect a progressive but nevertheless shallow uptrend in EURUSD through next year to 1.19 to reflect 1) a closure of the growth gap between the US and Euro area from 1.5% so far this year, and 2) a probable improvement in rate spreads in the euro’s favour as the ECB delivers rather more tightening than the curve prices. We continue to believe that delivery of early stage ECB tightening should be more impactful for FX than an extension of late-cycle Fed hikes as the market is liable to become more concerned about the longevity of the US cycle if the Fed is confronted.

After Italian spreads (10 year against Bunds) had climbed to 340bp on Friday morning they collapsed back to 300bp again. Only because EU Commis- sioner Pierre Moscovici seemed to find conciliatory words and explained the EU Commis- sion did not want to influence the economic policies of the Italian government. The euro also recovered in line with the Italian spreads.

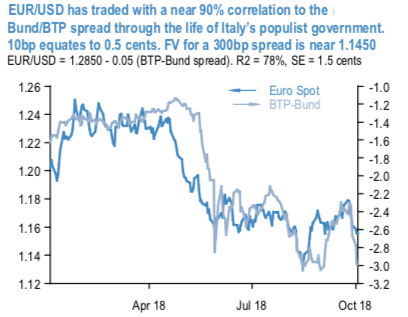

There has been an impressive degree of co-movement between EURUSD and the Italian risk premium ever since the previous Italian parliament was dissolved last December. The correlation through this period is close to 90%, dominated of course by the fraught period following the election in March as investors came to terms with an implausible coalition of populists and the euro sank by nine cents and the Bund/BTP leapt by 175bp (refer above chart). Courtesy: JPM

Currency Strength Index: FxWirePro's hourly EUR spot index is inching towards 36 levels (which is mildly bullish), while USD is flashing at 58 (which is bullish), while articulating at (08:15 GMT). For more details on the index, please refer below weblink: