Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different

AUDUSD remains in the middle of the USD 0.72 - 0.78 range that has held since mid-2016. The upside for the currency is indeed capped by the prospect of further narrowing in short rate spreads and a sense that the Australian economy is not performing as strongly as policy makers would probably like.

However, a move below USD0.72 in the near-term would require further escalation of China growth concerns and/or commodity weakness and a sense that the RBA has sufficient flexibility on the housing front to ease. As a result, AUDUSD is projected to decline further through 2017 on skinnier rate differentials and weaker terms of trade profile.

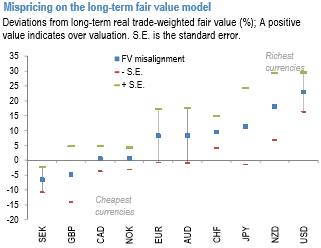

GBP has been in focus and has been the underperformer in G10 since our last publication in the run-up to the elections. The ranking hasn’t changed since our last publication, even though the dollar has continued to slide to make a new 6-month low on a TWI basis. Aussie and Kiwi dollar have still been the richest currencies, while SEK and GBP are still the weakest on the REER basis on this framework.

The valuation divergence has continued to persist in commodity currencies with NZD and AUD still screening rich vs. CAD and NOK. Valuations of petro-currencies are still near fair value (refer above chart), but still depressed from the long-run point of view.

CAD and NOK appear similarly near fair value but continue to appear quite cheap relative to Antipodeans (refer above chart), where valuations are still rich (refer above chart). NZD is the richer of the two currencies and appears richer-still given the outperformance in the past month.

Both currencies continue to face further downside in this framework as well in our forecasts, especially vs. EM high yielders as discussed in prior publications.