China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch

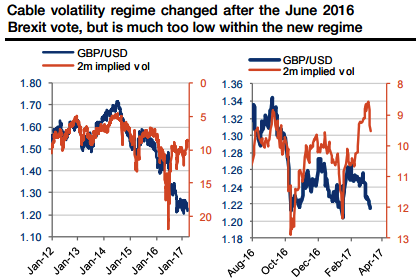

Cable volatility has been extremely directional since 2012, with a strong and stable negative correlation.

The Brexit vote in June 2016 initiated a new vol regime (unlike the FX/rates relationship which did not change throughout the event), as the currency massively depreciated while volatility did not rise in the same proportions (refer above graph).

Maintaining the previous regime would have required vol to stabilize above 15 with cable below 1.30, and realized vol did not support such high vol.

Importantly, such a break did not end vol directionality but instead reset it and shifted the relationship, once the option market had normalized in summer 2016.

Cable vol at 10 corresponded to approximately spot at 1.50 before mid-2016, and since then has been consistent with spot at 1.30.

However, the 2m implied vol has been too low since about one month, according to the prevailing regime (Graph 3b). With the GBP/USD at 1.20-1.22, volatility should be above 12 while most of the ATM curve is currently trading below 10. This is also consistent with the 2m realized volatility which is almost 2 vols above the implied (see above graph), involving a negative volatility risk premium. Implied vol is therefore much too low according to these metrics, in a context where the spot is getting dangerously close to the 1.20 low and macro uncertainty is still extremely elevated. The debate is now about what the long-term impact will be of triggering Article 50, not whether it happens or not. The 2m implied vol is currently undervalued by about 2 vols, and should pick up even more if cable accelerates below 1.20.

Unless an optional strategy involves a calendar spread, its profile will be convex in the region where it is long volatility (gamma and vega being positive together). In reaching the sub 1.20 uncharted territories, the spot is likely to depreciate in a disordered way, with possibly impaired liquidity (one-way market).

With volatility and skew both currently low, the option market would be taken aback and react in bidding vols. As such, we want to obtain downside convexity, which prevents selling low strikes or setting downside barriers. We are also unwilling to take topside unlimited risk (i.e. risk reversal profile).

As a result, we take advantage of the complacent vol and skew and recommend buying a 2m OTM cable put.