US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  Indian Government Bonds Seen Opening Steady Ahead of RBI Policy Decision

Indian Government Bonds Seen Opening Steady Ahead of RBI Policy Decision  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

With the deterioration in the local Turkish political situation and a less supportive environment from higher G3 yields, the outlook for the lira is worsening, in our view.

While the CBRT could conduct FX sale auctions or release FX liquidity from its FX liabilities like it did last week, we think the impact of these measures would be modest, and so we do not expect the central bank to be particularly proactive with its toolkit to stabilize the lira in the interim.

Following on from the economic coordination board meeting last week, we continue to receive conflicting signals from different policy camps: yesterday, PM emphasized during a speech that lira movements have necessitated a policy response, he emphasized that CBT would decide on its own measures.

President Erdogan's economic advisor Bulent Gedikli that past sharp rate hikes are the very reason why Turkey finds itself in its current state. This could mean that while the economic coordination board chaired by PM Yildirim agrees that rate hikes could be necessary, there has been no such agreement with President Erdogan's camp -- that would limit how far CBT will be willing to go with its lira defense via rate hikes. Our base-case is that CBT will raise rates modestly on Thursday, but that this will not have a lasting supportive effect on the lira.

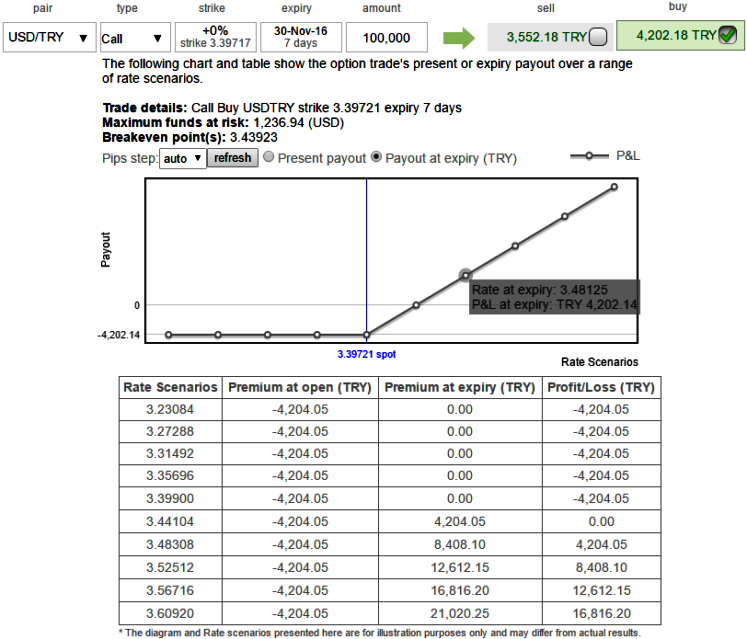

Please be noted that the ATM IVs of 1w and 1m are spiking crazily above 19% and 16.8% respectively. We find option exposures most attractive at present, with implied volatility and skew trading near their lowest levels in a year when we entered our USDTRY call on 7th November (USDTRY vol has recently spiked higher following the global risk-off after the US election results).

Going forward, the absence of local FX selling in the coming weeks could render USDTRY a lot more volatile than the market has grown accustomed to, in our view. The central bank has expressed concerns over the currency, suggesting it would not cut rates further without FX stability, but we doubt this is enough to stabilize the lira.

As a result, we recommend ATM +0.51 delta call options to mitigate further upside risks, why ATM contracts? Because the Vega is at its maximum when the option is ATM and declines exponentially as the option moves ITM or OTM. This is because a small change in IV will make no difference on the likelihood of an option far out-of-the-money expiring ITM or on the likelihood of an option far into-the-money not expiring ITM. ATM calls are far more sensitive since higher IV greatly increases their chances of expiring ITM.