Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns

Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch

Before we move onto the core of this write-up, please be noted that USDSGD has risen by around 2% since the start of June to around 1.3630, in line with the weakness in Asian currencies led by CNY’s drop, and the near term bias is still to the upside. The pair has tilted higher by 3% since early May, a hefty move compared to historical standards, yet in an orderly manner, which has allowed keeping realized vol (1M realized at 4.0vols) and, as reflect, implied vol (at 5.0vols) contained. Were trade tensions to unfold more abruptly, it would be natural to imagine a drop associated with higher realized volatilities.

Conversely, as discussed in the previous section, its “safe haven” status within the area, as for instance reflected by the lower interest rates (which normally call for higher vols), could support the choice of TWD as a candidate the short-vol leg of the trade.

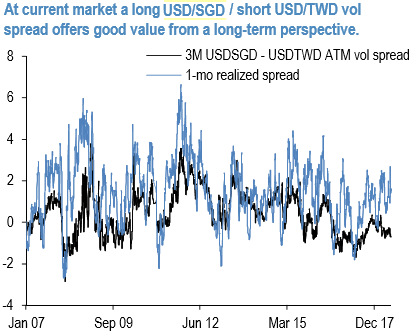

Currently, the Vol Carry embedded on the USDTWD front end of the curve is wider than for USDSGD. From a long-term perspective (refer above chart), the long USDSGD / short USDTWD vol spread offers value, given the favorable current level of Carry and the relative dynamics of realized volatilities; if we exclude episode of early 2011, realized volatility has usually spiked more violently on USDSGD than for USDTWD, thus supporting the long-vol leg of the RV trade. From a purely directional perspective, SGD might not be the optimal candidate for owning optionality and hedging a proper tail event in the region.

Owning optionality on a high-beta class would rather be preferred in an ideal scenario, with potential for high realized vol in a risk-off market. Despite not being a high-beta asset per se (if measured against moves in DXY or S&P Indices), the much higher betas of SGD relative to TWD support owning vol on the former rather than on the latter, putting aside idiosyncratic factors that could stimulate higher volatilities mostly on Taiwan denominated assets.

Thus, the carry-friendly nature of the trade combined with its modest downside risk offers a handsome risk-to-reward trade-off, thus stimulating the choice of SGD as the long-vol leg, despite the relatively contained potential in a bearish market. Also, given the idiosyncratic factors at play on TWD, suppressing directional sensitivities, the mean reversion potential of the trade is limited (as measured in terms of weak auto-regressive properties for the spread), which reduces the interest of adding Vega exposure via long-dated maturities.

On these grounds, compared to the earlier piece, we tend to favor the shorter (3M) end of the curve for increasing the sensitivity to the realized vol differentials, thus highlighting the carry-friendly nature of the vol trade rather than its pure hedge potential. This aspect of the USDSGD – USDTWD vol spread has been a potent P/L generator since 2016.

We advocate to Buy 3M ATM USDSGD straddles @ 5.025 choice vs short 3M USDTWD straddles @5.55/5.95 indic, both legs delta hedged, in vega neutral notionals. Courtesy: JPM