U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation

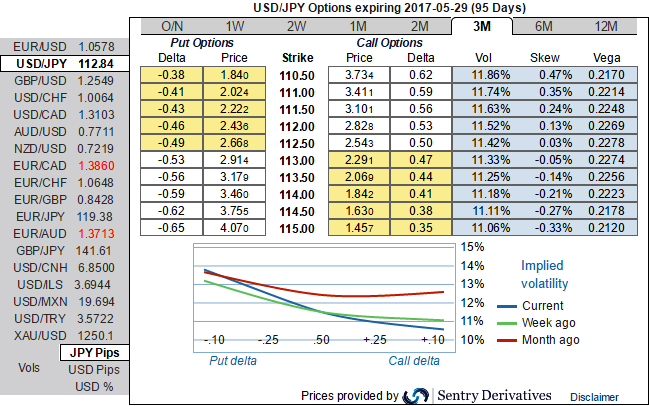

At spot reference: 112.89, USDJPY 3m risk reversals and IVs are indicating mounting hedging interests for downside risks (while articulating).

While 1m IVs have collapsed 16 points to 11.16% and 3m IVs are spiking at around 11.89%.

When IV increases and you are holding an option, this is good. Unfortunately, if you have sold an option, it is bad. Option writer expects IV to shrink away so the premium would fade away. You should also note short-dated options are less sensitive to IV, while long-dated are more sensitive.

The positively skewed IVs of 3m tenors are indicating the hedgers’ interest in OTM put strikes.

With bearish-neutral risk reversal, we wouldn't be surprised even if the underlying spot FX evidences the interim spikes, bears likely to drag again towards 112.169 and 111.450 levels sooner or later

Hence, we deploy ITM puts with longer tenors in our option strategy as the delta risk reversals favor bearish targets, hence in order to keep the risks on either side on the check we reckon diagonal debit put spreads are best suitable as the IVs and premiums are reasonable considering daily swings on technical charts.

So, here goes the strategy, Debit Put Spread = Go long 3m (1%) ITM -0.49 delta Put + Short 1m (1.5%) OTM Put with lower Strike Price with net delta should be at around -0.40.

For a net debit, bear put spread reduces the cost of trade by the premium collected (on the shorts of OTM put) and keeps option trader to participate in downward moves and any upswings in abrupt.

Glimpse over fundamentals: The fortunes of the dollar has been the dominant focal point of FX markets, with the dollar index down 2.2% over the past month, retracing nearly half of the post-election dollar rally into the end of last year on a reassessment of Trump policy expectations.

But dollar weakness in the past month has not been solely attributable to this. Positive data surprises and economic forecast revisions in the rest of the world make the US less exceptional and thus justify less strength in the USD, simply based on contemporaneous cyclical data.

The unwind of post-election dollar strength is now mature, judging from positioning indicators, short-term valuation models, and the price action itself. This suggests that while incoming information from Washington will continue to drive near-term broad dollar outcomes, that it may be less of a singular dominant driver, and that other macro developments outside Washington may take greater focus.