Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei

BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei  Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  RBI Hits Pause as Geopolitical Storm Clouds Gather

RBI Hits Pause as Geopolitical Storm Clouds Gather  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

Just as the market was craving any clear-cut statement on the Fed’s future interest rate policy in the run-up to the last FOMC meeting, regardless of how clearly they are staking out a rate rise in December. It simply brushes them aside.

The market is aware of the fact that there is still a considerable chance that this rate rise too will be postponed again - as happened so many times before. Should Donald Trump really emerge as the winner of the elections on 8th November the risks will no doubt rise again in the Fed’s view.

Concerns that could easily cause the Fed, and above all Fed chair Janet Yellen, to refrain from a rate rise with a reference to the uncertain (global) conditions. The market wants to avoid this trap. Hardly surprising therefore that there is certain indifference about the USD on the markets that remains unaltered by US data. That is unlikely to change short term.

OTC outlook and hedging frameworks:

Please be noted that the skewness in implied volatility of 3m tenors of this pair signifies the hedgers interest in OTM put strikes. While delta risk reversals of the similar expiries reveal more sentiments in hedging activities for downside risks in the similar tenors (3m expiries). This would raise a cause of concern that in this phase of time, the above stated major economic events are likely to intensify volatility in FX markets.

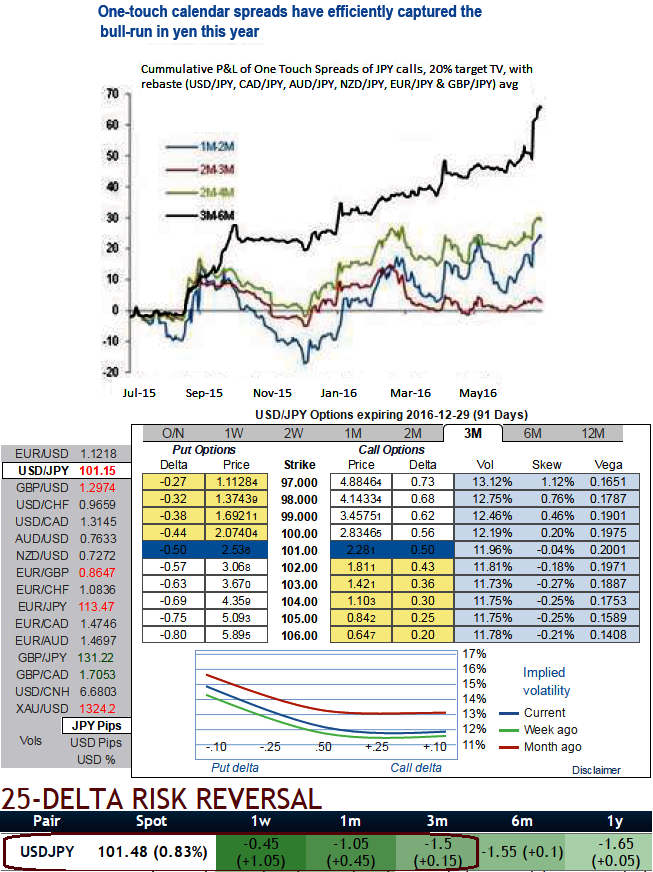

Vega-neutral USDJPY calendar spreads, on grounds that the vol curve is inverted in the 3M-1Y sector and that ex-BoJ day, realized vols are soft compared to ATMs (3M ATM 11.65 vs. ex-BoJ realized vol 10.5).

This class of trades has worked well for us this year given the persistent flatness of the yen curve, and we have often exploited the set up via one-touch calendar spread which is also a genuine directional alternative to straddle calendars in this instance.

The above chart shows that such structures have performed well in capturing the yen’s bull run this year, and function best on a basket of yen-crosses for short 3M vs. long 6M tenors.

Applied to USDJPY, this would suggest short 3M 94 vs. long 6M 94 one-touches that cost 13% to buy in equal USD notionals, and roll up to 25% in 3- months time should spot remain around current levels i.e. static carry gains of roughly 100% of the upfront premium.

The hope, of course, is to thread the needle by virtue of gentle yen appreciation over the next three months that stops short of breaching 95 – possibly as intervention concerns come to the forefront – and can lead to 2X-5X returns on upfront premium depending on terminal spot levels.