2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data

The fundamental forces contributing to the less pessimistic view of EURUSD now are threefold:

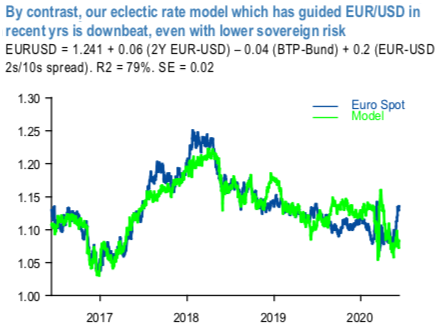

First, the proposals for a degree of fiscal burden sharing through the EU’s recovery fund (circa 5% of regional GDP spread over four years) have at the very least deferred the risk that a renewed wave of sovereign stress and/or populism in the periphery could compromise the integrity of the single currency once again, even if it is premature to conclude that this breakthrough definitively sets the region on the path to a fully-fledged fiscal union that would eliminate this existential tail risk once and for all. The recovery fund still faces opposition from the frugal four group of northern European countries and could yet be diluted in terms of a reduction in the 2:1 ratio of grants/loans (the EU Council meeting on June 19th is not expected to reach an agreement on the fund). The 70-80bp tightening in peripheral spreads have contributed 2-3 cents to the upgrade to the EUR forecast (refer 1st chart).

Second, the domestic political tail-risk to USD is increasing just as it is subsiding in the Euro area to judge from the narrowing in the odds on a Biden presidency and the potential for less-centrist policies under Biden compared to the pre-epidemic baseline.

Third, the market’s impressive/ blinkered (delete as appropriate) optimism about the global recovery could persist for a few more months yet as global data turns higher, before legitimate concerns about the quality and extent of the recovery are able to get a look- in; this optimism could continue to pressure USD generally and so support the desire of fund managers to neutralize long-standing EUR underweights.

But whereas these factors justify raising the EUR targets, we do not believe that they warrant an outright bullish trajectory for EURUSD. Crucially, the prospects for a sustained improvement in European growth remain highly contentious, so too therefore the possibility that EUR could repeat its 20 cents surge in 2017 when the Euro area temporarily took over as the engine of global growth (note that the ECB projects the economy to be 4% smaller by the end of 2022 than the pre-Covid baseline, even with its additional policy support).

Moreover, the post-Covid recovery in the global economy is also liable to remain incomplete (even without the risk of a second Covid wave) and so provide residual, medium-term support for USD irrespective of the Fed’s commitment not to hike until at least the end of 2022. The path to economic redemption, and hence a dramatically softer USD and stronger EUR, will be far more tortuous than either the post-Y2K experience when the USD REER shed 26%, or the post- GFC recovery when USD dropped 17%.

As things stand, EURUSD is already 1% above its 5Y average; for EUR to appreciate towards the 10Y average at 1.21 would likely require much greater clarity than investors currently possess about the durability of the global recovery, let alone the ability of the Euro area to more fully participate in this upswing than it has done in the past decade. Similarly, it is hard to imagine that the ECB will not maintain a looser monetary stance than the Fed for quite some time (the EUR curve prices only 10bp in hikes by mid-2024; the USD curve is double that). Negative rate differentials and the potential for excess QE will remain medium-term headwinds for EURUSD, we suspect. We expect the ECB to add another €750bn to PEPP in 4Q’20, to take its QE programme to a chart-busting 23% of GDP (refer 2nd chart).

Trading tips: At spot reference: 1.1243 levels (while articulating), although we see some cushion at 7 & 21-DMAs for today, contemplating short-term technical that indicates intraday selling sentiments, one can execute tunnel options spread strategy. Such exotic option with upper strikes at 1.1293 and lower strikes at 1.1168 levels likely to fetch exponential yields than the spot moves. The strategy can get assured yields as long as the underlying FX keeps dipping but remains well above lower strike.

Alternatively, we recommended shorts in EURUSD futures of July’20 delivery for the major downtrend, we now wish to uphold these positions on hedging sentiments. Courtesy: JPM