Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics

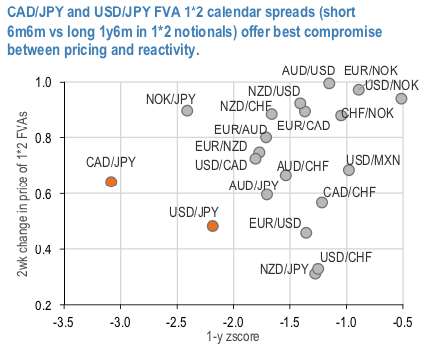

In this write-up, we emphasize on a strategy of FVA 1*2 spreads. Utilizing luring pricing and positive rolldown, 1x2 FVA spreads are time passage friendly and low maintenance long vega positions that struck us as a solid buy in the current environment where low decay vega is well sought after. The basic construct involves selling shorter-dated FVA along with an upward-sloping segment of the vol curve to partially fund the purchase of a longer-dated FVA that sits on a flatter part of the term structure. The roll-down of the short leg then compensates (or even eliminates, as is the case for CADJPY) the slide of the long position, all the while preserving the overall structure’s net long vol characteristic. The short leg is not large enough to disrupt the net positive sensitivity of the package to vol upturns.

Consequently, the structure is a carry efficient risk-off hedge. We screen for the FVA spread candidates based on their pricing (in form of a 1-y z-score) and the sensitivity to the ongoing market turbulence (in form of 2-week change in pricing of the package) – (refer 1st chart).

In the case of CADJPY, the current levels are still a bargain by historical standards, even after the recent bounce. The net 6-month static vol slide (at the expiry of the short leg) deteriorated as the front vols spiked on the back of the recent spot gyrations but is still positive thus making the long/short structure superior to holding a similar long-dated straddle (refer 2nd chart).

Consider short 6M6M CAD/JPY @8.7ch vs long 1Y6M @8.55/9.05, in 1:2 vega weights or short 6M6M USD/JPY @7.6ch vs 1Y6M @7.55/7.95 indic, in 1:2 vega weights. Courtesy: JPM