Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  BOJ Holds Interest Rates Steady, Upgrades Growth and Inflation Outlook for Japan

BOJ Holds Interest Rates Steady, Upgrades Growth and Inflation Outlook for Japan  Nasdaq Proposes Fast-Track Rule to Accelerate Index Inclusion for Major New Listings

Nasdaq Proposes Fast-Track Rule to Accelerate Index Inclusion for Major New Listings  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Elon Musk’s Empire: SpaceX, Tesla, and xAI Merger Talks Spark Investor Debate

Elon Musk’s Empire: SpaceX, Tesla, and xAI Merger Talks Spark Investor Debate  Federal Reserve Faces Subpoena Delay Amid Investigation Into Chair Jerome Powell

Federal Reserve Faces Subpoena Delay Amid Investigation Into Chair Jerome Powell  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary

Vey recently many voiced surprising tone at this juncture about the JPY weakness. Neither the recent Bank of Japan’s recent measures to cap long-term yields close to zero nor BoJ governor Haruhiko Kuroda’s dovish comments was entirely new. Why did the market react the way it did?

The central banks in G7 nations are lined up to announce monetary policy announcements, BoC on 12th July, BoJ and ECB on 20th July, FED on 26th July and BoE on 3rd Aug.

It was not the first time when the BoJ announced an auction last Friday at which it would buy unlimited bonds at a fixed yield. It is its self-set objective, which it first announced in September last year, to keep the yield curve at -0.1% at the short end and at 0% at the long end. None of that is indeed new.

However, what is new is the global monetary policy environment. An end of the expansionary monetary policy is being discussed almost everywhere. The ECB is likely to announce a further tapering of its asset purchasing programme before the end of the year and the markets are pricing in a first rate hike for next year.

Also, the Bank of England is likely to raise interest rates soon in the view of the markets. And the market even expects to see the Bank of Canada to start a rate reversal tomorrow. Even Riksbank and Norges Bank have recently dropped their easing bias (i.e. the reference to a possibly more expansionary monetary policy) and are thus slowly but surely moving towards an exit.

Of course, the BoJ does not deviate completely from this trend. BoJ governor Kuroda has already admitted openly that the central bank probably will not reach its bond purchasing target of JPY 80 trillion this year.

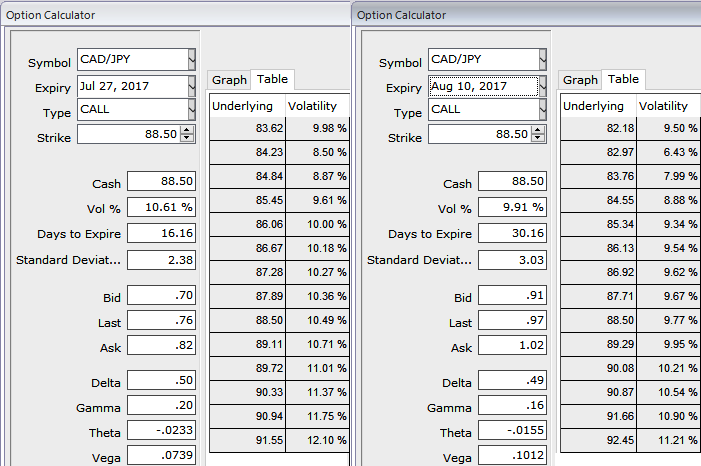

OTC outlook and options strategy:

Please be noted that call options of 1m and 2m tenors are trending higher at 9.16 and 9.34% respectively.

Please also be noted that the options with a higher IV cost more which is why in this case OTM puts have been preferred over ATM instruments. This is intuitive due to the higher likelihood of the market ‘swinging’ in your favor. If IV increases and you are holding an option, this is good.

Well, in order to arrest this upside risk that is lingering in intermediate trend and prevailing declining trend, we recommend diagonal option strap versus OTM put strategy that favors underlying spot’s upside bias in long run and mitigates bearish risks in short term.

So, we recommend building the FX portfolio exposed to this pair with longs positions in 2 lots of 1M ATM 0.51 delta calls and 1 lot of ATM -0.49 delta puts of 2w expiries.