RBI Hits Pause as Geopolitical Storm Clouds Gather

RBI Hits Pause as Geopolitical Storm Clouds Gather  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Indian Government Bonds Seen Opening Steady Ahead of RBI Policy Decision

Indian Government Bonds Seen Opening Steady Ahead of RBI Policy Decision  Indonesia Passes New Central Bank Law, Raising Investor Concerns Over Policy Independence

Indonesia Passes New Central Bank Law, Raising Investor Concerns Over Policy Independence  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

In the recent unanimous decision of South African central bank (SARB), benchmark rate is unchanged at 7% as had universally been projected. However, the SARB increased its projections and now only expects the overall rate to return into its target corridor of 3% to 6% by late 2017 (previously Q2 2017).

In addition to the higher oil price, this is mainly due to the strong rise in food prices as a result of the drought, that is taking longer to return to normal than expected.

The SARB now expects an average of 6.2% for 2017, following previously 5.8% while it still expects 5.5% for 2018. It has only lowered the growth forecast for 2017 marginally to the downside to now the moderate growth of 1.1% for 2017 (previously 1.2%) and 1.6% for 2018. The SARB seemed worried about the deteriorating short-term inflation outlook as well as about the fact that based on its calculations inflation will remain too close to the upper end of its target range even longer term.

However, it once again stressed its willingness to raise interest rates further should second round effects emerge. USDZAR eased further yesterday. Let us point out at this juncture that the rand remains susceptible. South Africa is still at risk of being downgraded to junk status, if the rating agencies consider the progress made with the reform efforts and stabilizing of the budget to be insufficient.

While the changed political landscape suggests the medium-term picture is shifting more positive, we remain tactically bearish ZAR.

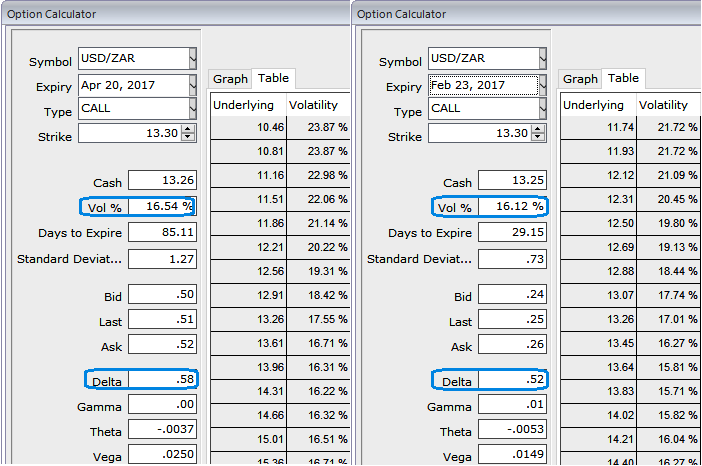

Subsequently, on the option trade front among EMFX, we recommend positioning longs in USDZAR as the South African significantly overshooting fundamentals –

Please note that 1-3m IVs are conducive for call spreads, thus, advocating longs in USDZAR portfolios that make us buying USD vols all the more appealing. Instead of naked vanilla call form, we suggest call spread structure for the 2M horizon, optimizing strikes for leverage.

In USDZAR, the 1M-2M ATM spread is below average at +0.75, as 1M vols had remained relatively anchored and never softened significantly.

Therefore, the premium for owning US elections risk isn't punitive, and the short leg further mitigates the cost of gamma.

The above table explains how does the call spread is ordered in decreasing values of max payout/cost.

We find that skews aren’t steep enough vs ATM to allow for a wide range of strikes to be efficient. In order to ensure more than 50% discount to the outright vanilla, and a max payout/cost higher than 3.5:1, one needs to choose a combination of long 40D vs 25D.

The call spread achieves a 55% discount to outright call and a max payout/cost ratio of 3.7:1 (mid values).