Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

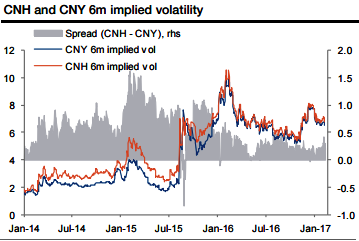

The options trades are preferable over forwards as the implied volatility is similar between CNH and CNY (CNH vol is 0.2 vol points higher than CNY vol in the 6m tenor) and the vol spread has been narrowing over time.

These conditions provide interesting option-based relative value strategies, where investors can enter zero cost structures (plus/minus a few basis points depending on spot, points, and vol) to position for the CNH-CNY basis flipping.

A notable advantage of the option strategy is that positioning for the basis to flip is contingent on RMB depreciation (topside strikes), whereas a position in forwards could underperform and has greater MTM risk if the RMB strengthens or is stable.

Our base-case scenario envisions USDCNY rising to 7.30 by the end of 2017. The structural richness of implied volatility over realized argues for short volatility structures. Additionally, short downside volatility is appealing because there are few fundamental reasons for the CNH to trade meaningfully stronger over the next year. Owning a 1yr USDCNH zero-cost seagull structures have consistently been advocated (6.90/7.20/7.50, zero cost) offers a maximum gain of 4.1%. With no digital risk involved and limited convexity, the position can be conveniently delta-hedged. Losses are unlimited if USDCNH trades below the 6.90 strike in one year.

The structure is a standard 1y call spread strikes 7.20/7.50 fully financed by selling a put strike 6.90, exposed to a maximum USDCNH appreciation of 4.1% at expiry.