Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

A revised Brexit deal was agreed jointly by the UK and EU yesterday, but without the blessing of the DUP, this does not mean that the no deal risk has disappeared. Tomorrow’s decision by Parliament might not only decide whether this deal is going to be the one. The President of the Commission Jean-Claude Juncker made it as clear as possible repeatedly yesterday that there would be no further extensions - if Parliament were to reject this deal. The result would be a no deal Brexit at the end of the month. Take it or leave it.

Admittedly, the sly old fox Juncker is often a lot of talk and no action. Perhaps he just wants to put pressure on the UK Parliament. Without pressure - that much we have worked out over the past few years - they can’t even agree on what the time is. And in the end it is not Juncker’s Commission but the Council that has to decide about an extension.

Nonetheless: if the UK MPs were to reject the deal tomorrow the FX market would have to think long and hard as to whether the 5¼% GBP appreciation (against USD) would have to be retraced. In that case it would have to be considered whether additional GBP weakness would be justified, as a no deal risk would then be higher than last week (before the GBP positive news began to emerge).

The FX market is right to continue to reflect this imbalanced risk in a lopsided vol surface. EURGBP calls are much more expensive than EURGBP puts. That makes sense as in the positive case - if Parliament passes the deal tomorrow - quite a lot has already been priced into the GBP spot levels.

Nonetheless: Compared to what could happen in case of a no deal the volatilities remain low. An (annualized) 1-month ATM vols around 11.6% for example implies EURGBP moves of less than 3.4% over the month. If we were to see a no deal scenario much more than that would be likely. Anyone who holds non-diversifiable GBP risks will therefore have no choice but to maintain their hedging.

As that is the case we might see a sudden increase in demand for GBP next week. That means that also at the lower end in EURGBP not enough GBP volatility may be priced in yet on the options market.

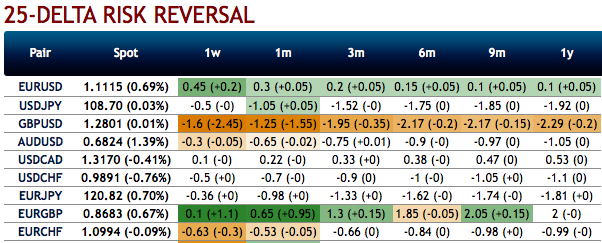

Take a quick glance at FX OTC outlook before looking at the options strategies. Fresh positive numbers are added to bullish risk reversals of EURGBP. This is an indication of the broader hedging sentiment for the bullish risk outlook in the FX OTC markets, this is interpreted as the hedgers are keen on bullish risks but with the mild downside risk sentiment in the near-term (refer to negative risk reversals in 1m).

While the passively skewed IVs of 3m tenors are stretched are indicating upside risks, more bids are observed for OTM call strikes up to 0.8850 level.

While EURGBP risk reversals of the existing bullish setup remain intact with mild bearish shift, you see minor negative risk reversal numbers, but it should not be perceived as the bearish scenario changer. Instead, below options strategy could be deployed amid the expected turbulent condition.

According to the OTC FX surface, 3-way options straddle versus ITM calls are advocated seem to be the most suitable strategy for EURGBP contemplating some OTC sentiments and geopolitical aspects.

Options Strategy: The strategy comprises of at the money +0.51 delta call and at the money -0.49 delta put options of 2m tenors, simultaneously, short (1%) ITM calls of 1w tenors. The strategy could be executed at net debit but with a reduced trading cost.

Hence, on hedging as well as trading grounds, initiate above positions with a view of arresting potential FX risks on either side but slightly favoring short-term bearish risks. Courtesy: Sentrix, Saxo & Commerzbank