US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks

BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  RBI Holds Interest Rates at 5.25%, Cuts India Growth Forecast Amid Rising Global Risks

RBI Holds Interest Rates at 5.25%, Cuts India Growth Forecast Amid Rising Global Risks  BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

BOJ Raises Interest Rates to 1% as Inflation Pressures Persist  Indonesia Central Bank to Draft New Regulations After Expanded Economic Growth Mandate

Indonesia Central Bank to Draft New Regulations After Expanded Economic Growth Mandate  ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

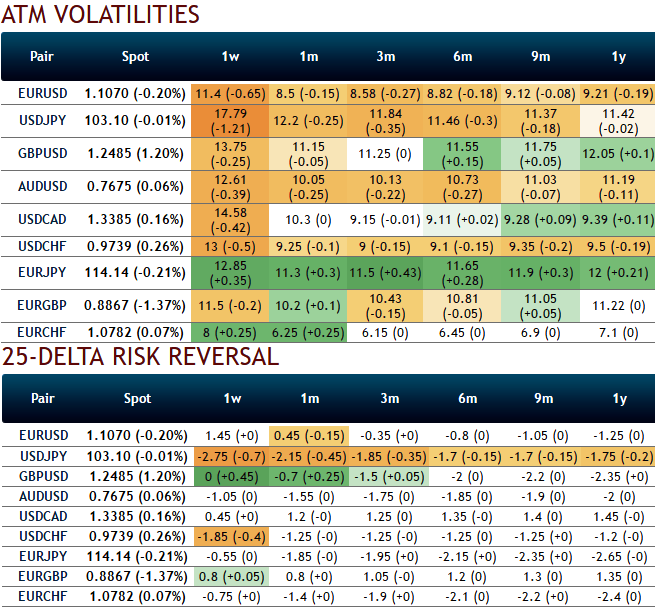

OTC updates:

As per the nutshell showing implied volatilities and delta risk reversals, USDJPY is rising higher IVs of 1w tenors with hedging sentiments for downside risks in the tenor which is the highest among G10 currency space. While the long-term hedging arrangements for downside risks still appear to be intact. Hence, we recommend below option strategy so as to match the above fundamental as well as the OTC scenarios.

While USDJPY pin risk is seen in options expiring on this Friday at strikes 100.95, most importantly, as the OTC VIX USDJPY is the pair to have highest volumes.

VXY indices have barely moved on the week, however, demonstrating once again that the linkage between USD spot and vols has broken down.

In fact, the VXY G7 index would be down were it not for USDJPY vols lifting up 0.5vol on higher spot - in spite of the sign of the USDJPY risk-reversal being negative (see above nutshell showing further down, where we assess that the fair value of 3M RR 25D USDJPY should be flat based on spot-vol betas).

By this we mean FX Options strikes in large notional amounts, when close to the current spot level, can have a magnetic effect on spot prices. That is, the spot may trend around those strikes as the holders of the options will aggressively hedge the underlying delta.

Fundamental outlook:

On the data front, the BoJ to maintained status quo at this MPM as widely expected despite the downward revision to the inflation outlook.

PMI, Shoko Chukin small firm survey, and real exports confirmed the manufacturing is gaining momentum.

The consumption stopped decreasing in September and is expected to rebound in Q4.

CPI trend inflation in Japan continued to decelerate in part due to the lagged effect of yen appreciation.

The currency could weaken significantly if expectations overseas for inflation pick up and moderate growth of around 2 pct in the U.S. can be achieved, facilitating Federal Reserve rate increases.

Option Trade Recommendation:

The spot reference of USDJPY is at 103.271, the least since 12th October. So if the market is blissful to add longs in USDJPY as a positively convex play on the BoJ meeting, the result of such demand is that USDJPY is now 2% expensive compared to the 10Y rate spread.

Well, on hedging grounds, hold a USDJPY put fly (104.777 x 103.271 x 102.388 in 1x2x1 notional) with 1w expiry.