RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200  Indonesia Passes New Central Bank Law, Raising Investor Concerns Over Policy Independence

Indonesia Passes New Central Bank Law, Raising Investor Concerns Over Policy Independence  Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

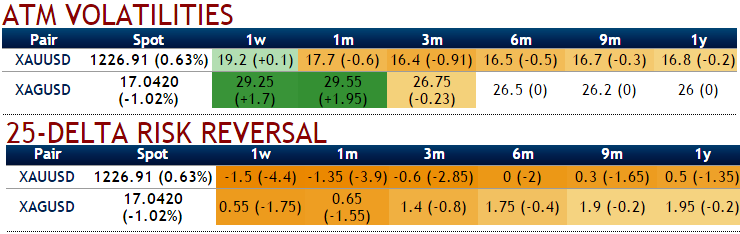

The ATM IVs of silver of 1w-1m expiries are spiking higher crazily, 1m IVs are shy above 29.50% that encompasses Feds rate hike speculations (as we get closer to December, the investors are currently pricing higher chances of a rate hike at the Fed's December monetary policy meeting).

While extremely negative delta risk reversal flashes higher numbers that signify OTC bullion is more concerned about bearish risks of silver prices in this course of time.

On the Comex, silver prices for December delivery rose 9.0 cents, or 0.53%, to $16.98 a troy ounce during morning hours in London, bouncing back after dropping to $16.62 on Monday, the lowest since June 8.

Since 1m IV is on the higher side with extremely bearish hedging sentiments, it implies that the bullion market reckons the price has more potential for large movement southward direction. The precious metal is sensitive to moves in U.S. rates, which lift the opportunity cost of holding non-yielding assets such as bullion while boosting the dollar in which it is priced.

Additionally, the momentum in bear trend is gaining more traction, but from the last couple of weeks the strength amid growing concerns over global risk sentiments, this sentiment is now changing.

Hence, as shown in the diagram, hence, we recommend initiating longs in 2 lots of 1M ATM +0.51 delta call, and simultaneously short 1 lot of ITM call (1%) with comparatively shorter expiry in the ratio of 2:1.

We encourage -0.49 ATM delta puts in our strategy, as the ATM contracts are more expensive and gamma/vega sensitive than OTM contracts, but cheaper than ITM options. They have the highest Gamma, Vega, and Theta which means their premium is the most sensitive to moves in either direction.

So, trading option spreads in ATM and ITM strikes allows the traders in many puzzling market scenarios and likely to fetch not only positive cashflows as you could see the payoff structure but also the cost advantage.

The higher strike short puts seems little risky but because IV responds adversely (bets on RR and current downswings in underlying price to prevail), the likelihood of options expiring in the money is very less and it finances the purchase of the greater number of long puts (ATM calls are reasonably priced, so we loaded up with the weights in the spreads) and the position is entered for reduced cost.