Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data

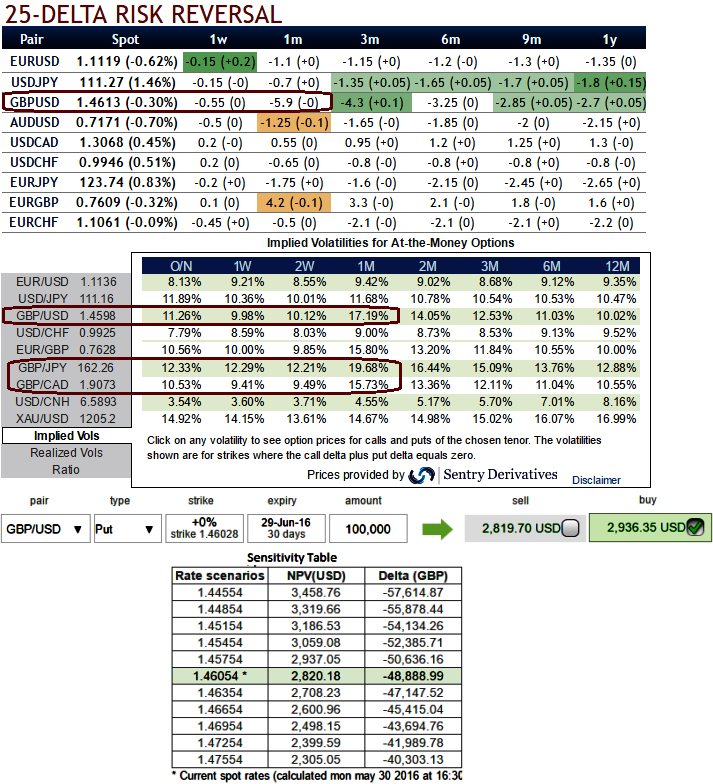

After previous monetary policies from ECB, Fed and BoE, the euro and sterling OTC market turbulence was cooling off, as the hedging sentiments for certain currency pairs have been losing the traction.

The focus this week turns to the ECB and the Fed. The ECB will not take any fresh action but the press conference will be interesting for views on its reaction function as inflation forecasts start rising.

The ECB may also consider reinstating the collateral waiver on Greece. In the US, we expect a weak non-farm payrolls number for May which would increase the hurdle for the Fed to hike in June.

Ahead of UK's PMIs in this week, sterling gained against the majors except Euro, GBPUSD was up almost 0.13% at 1.4607 from the lows of 1.4587 earlier European session.

In this month, GBPUSD with BoE's unchanged bank rates at 0.5% were already factored in as it was much anticipated move that kept sterling away from much of hedging activities.

But for now, the implied volatilities flashed screaming off as the sterling crosses surged because UK PMIs are likely to indicate prospects of their economic health - businesses react quickly to market conditions and Fed is on the focus during mid June. UK referendum is on the other corner that appends sizeable risks to sterling.

1m IVs of GBP crosses are observed to have spiked massively considering above event risks, highest among G10 currency space.

While, risk reversal numbers are also flashing highest values that indicates the hedging instruments getting expensive in OTC markets anticipating downside risks.

We stated in our previous write up as well that the vols in OTC are likely to pick up rapidly again in 1-3M tenors as these tenors encompasses all significant data events.

The above table ranks in rising implied volatility among G10 currency crosses, sterling overreacting due to upcoming economic events but likely to tumble and stabilize at 12.5% in coming months. IV and risk reversal readings of GBPUSD have been the best buys on for selecting put options.

Hedging bets:

Let's now consider ATM GBPUSD put options of 1m tenors, they are trading at just shy above 4.11%.

While delta risk reversals are still flashing up progressively with positive numbers that favours bulls and indicates they are willing to pay OTM strikes in higher vols.

Since, IVs of ATM contracts are at higher levels with negative risk reversals would mean that puts have been underpriced relatively to the calls.

During Brexit scenario, at spot FX of GBPUSD is trading at 1.4603, and is anticipated to tumble moderately in the months to come, so it is better to use near month at the money puts with 50% delta in any hedging strategies.