US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

The dollar rally continues and the expected pause has yet to materialize. Meanwhile, the Turkish central bank has raised rates by 300 basis points to stem the slide in the lira, but even this move could prove insufficient.

The sell-off in Italian bonds continues and is increasingly spreading to the other market segments. Although we expect continued selling pressure, a self-reinforcing escalation similar to 2011 seems unlikely. 10y Bund yields should nonetheless continue to struggle below the important 0.50% mark.

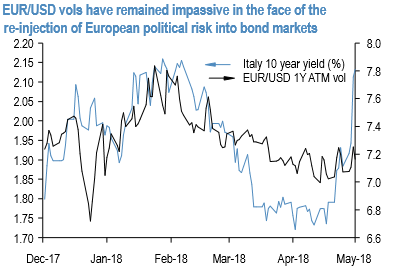

6M-1Y EURUSD ATM vol good value after re-emergence of Italian political stress: The EURUSD vol surface has appeared low and flat over the past few months, and especially cheap relative to the widening of forward points to unprecedented highs.

Despite their obvious value, a catalyst for mean-reversion in Euro vol had been difficult to pinpoint even through the ongoing turmoil in EM, especially after directional EUR call option demand – so influential in driving a mini vol surge in 3Q’17 – cooled off earlier this year alongside the bull-momentum in the spot.

The re-emergence of European political risk (Italy) over the past two weeks has finally supplied the missing piece of the jigsaw that in our view should serve to push portfolio hedgers off the fence towards a more active embrace of EUR vega in coming weeks.

Mid-to-long (6M-1Y) expiries, in particular, have remained strangely impassive in the face of the 40bp sell-off in BTPs from their lows (refer above chart) and are better value than shorter tenors along a now inverted 1M/1Y vol curve. Political uncertainty can also drag on for longer than short-dated options can withstand, and 6M expiries in particular that span the US midterm elections do not appear to price in much risk premium for the event (6M3M ATM spread 0).

A final factor supporting EUR vega ownership is the possibility of European asset managers partially switching to option-based FX hedging programs over the next few months as negative carry on standard forward based hedging programs has become too punitive; conversations with accounts suggest an inclination towards buying EURUSD call spreads to partially replace forwards and in the process reduce portfolio exposure to the double whammy of simultaneous losses on overseas assets as well as the FX hedge (both SPX and EURUSD crashed in 2008).

While timing and notional sizes of any such hedging related option uptake are difficult to quantify ex-ante, the possibility of a new source of investor demand in coming months creates asymmetric upside risks to EUR vol from current historically depressed levels. Courtesy: JPM

FxWirePro launches Absolute Return Managed Program. For more details, visit: