Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit

Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit  Smartphones are helping filmmakers tell the stories the movie industry overlooks

Smartphones are helping filmmakers tell the stories the movie industry overlooks  Buy the Dip: Gold Holds Strong at $3980, Targets $4150

Buy the Dip: Gold Holds Strong at $3980, Targets $4150  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails

Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails  Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027

Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand

Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand  Trump has made more than $1 billion from crypto in a year. How?

Trump has made more than $1 billion from crypto in a year. How?

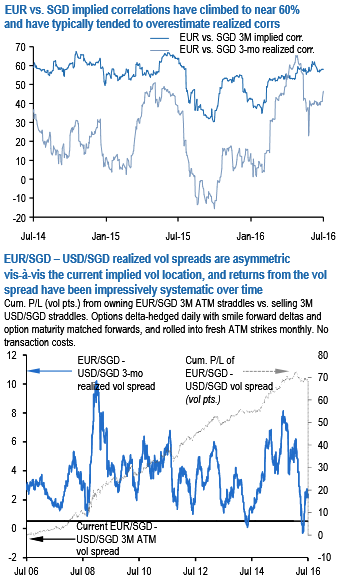

Long EUR/SGD vs. short USD/SGD gamma spreads form a classic relative value set-up with excellent entry levels, asymmetric payout profile and a long history of return outperformance. EUR vs. SGD implied correlations have recovered smartly from their Q1 lows towards 60%, and odds are that future realized corrs will fall short of this high bar as they have usually done in years past.

A direct corollary of this correlation set-up is that EUR/SGD – USD/SGD implied vols have fallen to multi-year lows, from where returns on the gamma spread are biased asymmetrically higher given the recent as well as the long run history of realized vol behavior (see chart).

The above chart also best reflects the persistent underperformance of EUR vs. SGD correlations in the form of impressive Sharpe Ratios from owning EUR/SGD vs. USD/SGD straddle spreads, indicating a degree of structural underpricing of EUR/SGD cross vols that is also shared by EUR-cross vols against other regional currencies such as KRW and INR.

While the precise cause is unclear, vega-supplying retail structured products might have a role to play in this, not dissimilar to the effect of higher profile Uridashis on JPY-cross vols spread is net time decay positive, and offers exposure to the idiosyncratic risk of INR volatility stemming from the RBI governor change and the specter of FCNR outflows.