In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  AI can be a personal trainer in your pocket – but is it safe?

AI can be a personal trainer in your pocket – but is it safe?  Vietnam’s population hit the 100 million milestone. Where’s it headed?

Vietnam’s population hit the 100 million milestone. Where’s it headed?  Gold Pulls Back After Hitting $4,180 as Geopolitical Risk Sends Crude Higher

Gold Pulls Back After Hitting $4,180 as Geopolitical Risk Sends Crude Higher  Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027

Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027  Bernstein Names IAG, Ryanair as Top European Airline Stocks Ahead of Earnings

Bernstein Names IAG, Ryanair as Top European Airline Stocks Ahead of Earnings  Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails

Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails  USA at 250: the Black American struggle for life, liberty and the pursuit of happiness

USA at 250: the Black American struggle for life, liberty and the pursuit of happiness  State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’

State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026

JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026  Goldman Sachs Flags 3 Key Risks Ahead of Europe’s Earnings Season

Goldman Sachs Flags 3 Key Risks Ahead of Europe’s Earnings Season  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  Bank of America Upgrades T-Mobile to Buy, Says LEO Satellite Fears Are Overdone

Bank of America Upgrades T-Mobile to Buy, Says LEO Satellite Fears Are Overdone

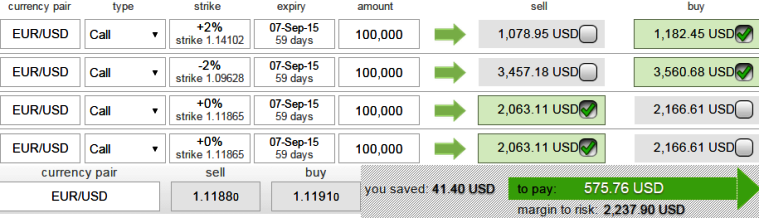

For those who don't like to accumulate either existing shorts on EUR positions or not longs dollar side with minimal delta terms, instead, better to take long term neutral positions such as option butterflies. We have some smart trading arrangements; these can even be utilized in our model the assortment of portfolio until the better clarity on how these global factors (especially Greece on euro side & Fed's decision on dollar side) will play out.

Therefore, buying 2M (+2%) Out-Of-The-Money (strikes at 1.1412) 0.34 delta call, buy another 2M (-2%) In-The-Money (strikes at 1.0964) 0.67 delta call and simultaneously sell 2 lots of 2M At-The-Money calls with positive theta values. All the positions should be early September maturities. As the delta on butterflies would usually be zero, this option combination should also be close to zero.

We reckon, this butterfly spread is best suitable and enables market laggards, risk averse traders, speculators who've been bias on both Fed's hike news and Grexit matters to participation in market turbulence as it brings in limited returns and limited risk.

Hedgers whose is neutral on irrespective market making matters but involved with their international business, this would arrests systematic risks.

Long butterfly spreads are entered when the investor thinks that the underlying exchange rate will not rise or fall much by expiration. One additional long position would result in net debit.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: Laggards who expect Fed’s hike in September hedge EUR/USD using long butterfly

Friday, July 10, 2015 12:33 PM UTC

Editor's Picks

- Market Data

Most Popular