China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Retail sales in New Zealand increased 1.1 pct on quarter in the three months to June 2018, following an upwardly revised 0.3 pct rise in the previous quarter. Faster growth was mainly explained by: department stores (+2.8 pct vs 0.0 pct in Q1); hardware, building & garden supplies (4.7 pct vs 0.6 pct); recreational goods (4.9 pct vs -0.4 pct); accommodation (3.2 pct vs 1.9 pct).

Consequently, Kiwis dollar surged considerably, NZDUSD rose from 0.6660 to 0.6701. While AUDNZD fell from 1.1050 to 1.1007, NZDJPY 73.844 to 74.081 levels.

Bearish NZDJPY scenarios:

1) The NZ housing market slowdown becomes disorderly

2) The NZ immigration rolls over quickly

3) NZ bank funding issues intensify, causing the market to question NZ's ability to attract capital inflow.

Bullish NZDJPY scenarios:

1) Fiscal easing is delivered quickly

2) New RBNZ Governor Orr starts with a surprisingly hawkish bent.

Over 2018, we see scope for some further under- performance from NZD, as we expect ongoing confirmation that the RBNZ can credibly lag policy normalization in the G3. Evidence that real assets (equities, housing) are threatened by late cycle growth dynamics and government intervention would add further weight to this story.

Markets are now pricing a small chance of an RBNZ easing by early next year. At the June decision RBNZ Governor Orr maintained an evenly balanced outlook for the near-term, with addition of downside risks. The Governor stated the next rate move is equally likely to be up or down, and has placed significant weight on the fact that inflation expectations have become more backward-looking, which slows the recovery from several years of below target outcomes.

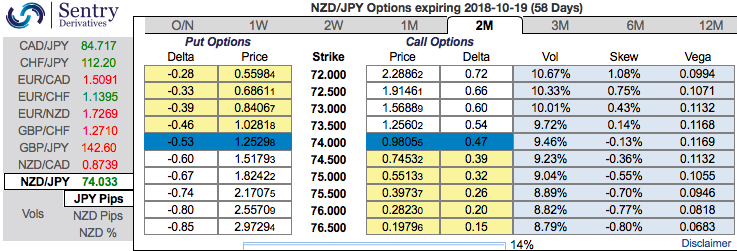

NZDJPY’s trend has been within the tight range of 76.859 – 74.040 levels, but the pair is having more bearish traction and expected to depreciate upto 72.5 levels by 3Q’19 as RBNZ outlook remains on hold throughout 2018.

To substantiate this bearish stance, the 2m positively skewed implied volatility indicates the hedging sentiments for the lingering bearish risks. Bids are for OTM puts upto 71.500 levels.

Implied volatilities of this pair is trending at 8.02% and 8.67% of 2w and 2m tenors respectively. Lower IVs are conducive for options writers and higher IVs are good for option holders.

As a result, we construct suitable options strategy favoring slightly on bearish side. Initiate 2 lots of 2m longs in -0.49 delta put options, simultaneously, short 1 lot of (1%) put options of the narrowed expiry (preferably 2w tenors), the strategy is executed at net debit.

The short side likely to reduce cost of hedging with time decay advantage on short leg, while delta longs likely to arrest potential bearish risks.

Currency Strength Index: FxWirePro's hourly NZD spot index is inching towards 65 levels (which is bullish), while hourly JPY spot index was at -25 (mildly bearish) while articulating (at 06:05 GMT). For more details on the index, please refer below weblink: