Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data

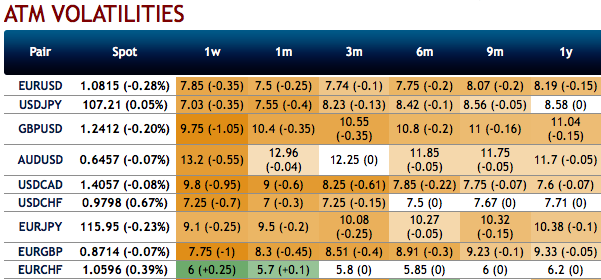

Among the three bearish drivers of FX in March economic fallout from COVID-19, oil price war and poor liquidity only one has abated (oil).

The weak fundamentals keep us cautious in FX. Growth forecasts are still getting downgraded, even though new infections have peaked in DM. FX markets remain asymmetric to vol shocks.

ATM IVs (implied volatilities) of G10 FX-bloc has again been dipping (refer above nutshell), the sharp reversal in the VXY in April series has left it screening 0.5 - 1.5 pts. cheap vs. cyclical correlates, which is hard to justify in a climate of worsening growth, elevated oil / commodity volatility and political tails risks in Europe and China.

GBP, Scandi FX downgraded as you could observe the negative bids for the existing bullish risk reversals, while euro crosses see upside hedging and CAD also sees upside hedging sentiments.

Mid-curve USDCAD vols screen cheap despite the dramatic sell-off in oil this week. Buy USD call/CAD put one-touch calendar spreads with premium rebate as a carry-positive, leveraged forward volatility play.

The increase in hawkish rhetoric of late out of the US around China in the context of COVID-19 risks another flare-up in US/China tensions. Buy low and flat CNH 6M6M forward volatility (FVA) as a hedge, which has the added benefit of offering pre- vs. post event exposure around the US elections in November. Courtesy: JPM & Saxo